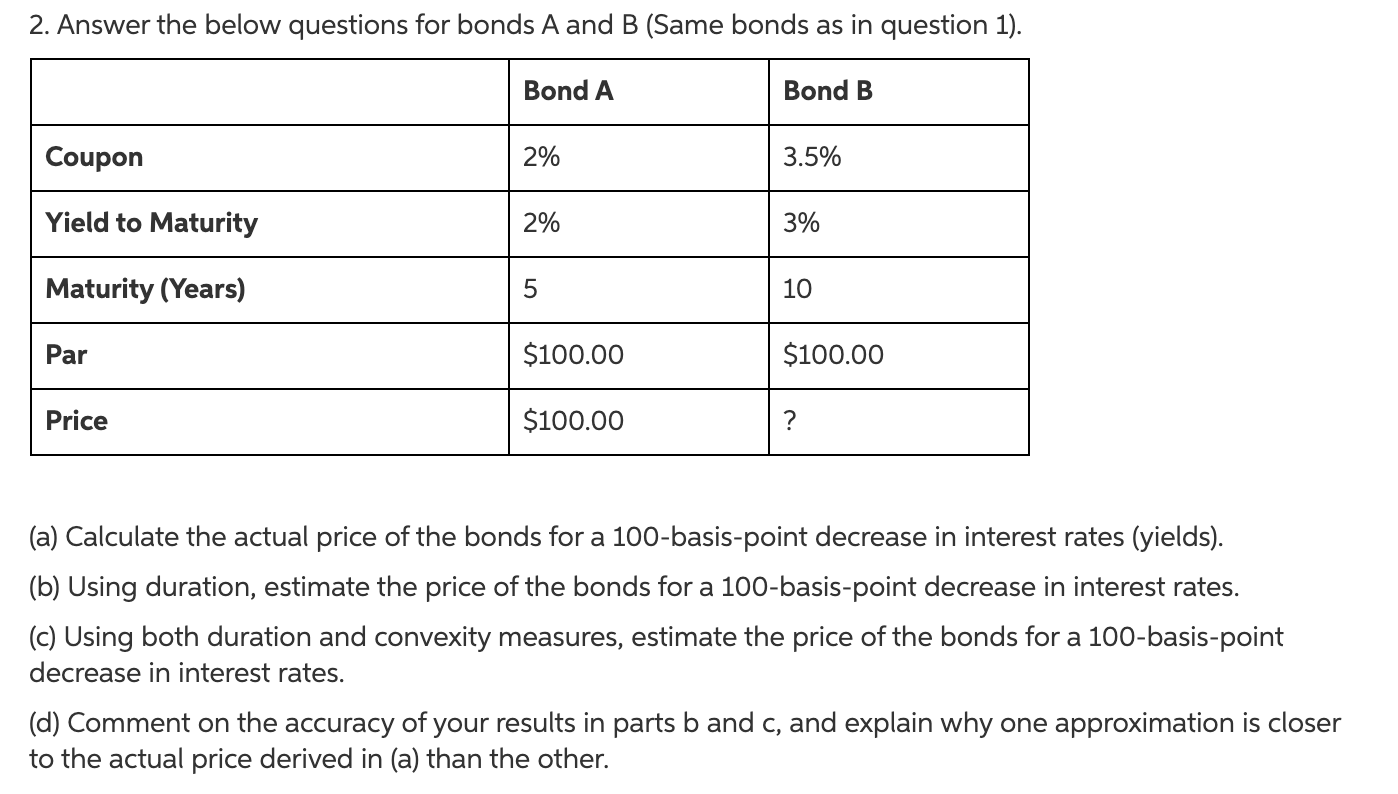

Question: 2. Answer the below questions for bonds A and B (Same bonds as in question 1). Bond A Bond B Coupon 2% 3.5% Yield to

2. Answer the below questions for bonds A and B (Same bonds as in question 1). Bond A Bond B Coupon 2% 3.5% Yield to Maturity 2% 3% Maturity (Years) 5 10 Par $100.00 $100.00 Price $100.00 ? (a) Calculate the actual price of the bonds for a 100-basis-point decrease in interest rates (yields). (b) Using duration, estimate the price of the bonds for a 100-basis-point decrease in interest rates. (c) Using both duration and convexity measures, estimate the price of the bonds for a 100-basis-point decrease in interest rates. (d) Comment on the accuracy of your results in parts b and c, and explain why one approximation is closer to the actual price derived in (a) than the other

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts