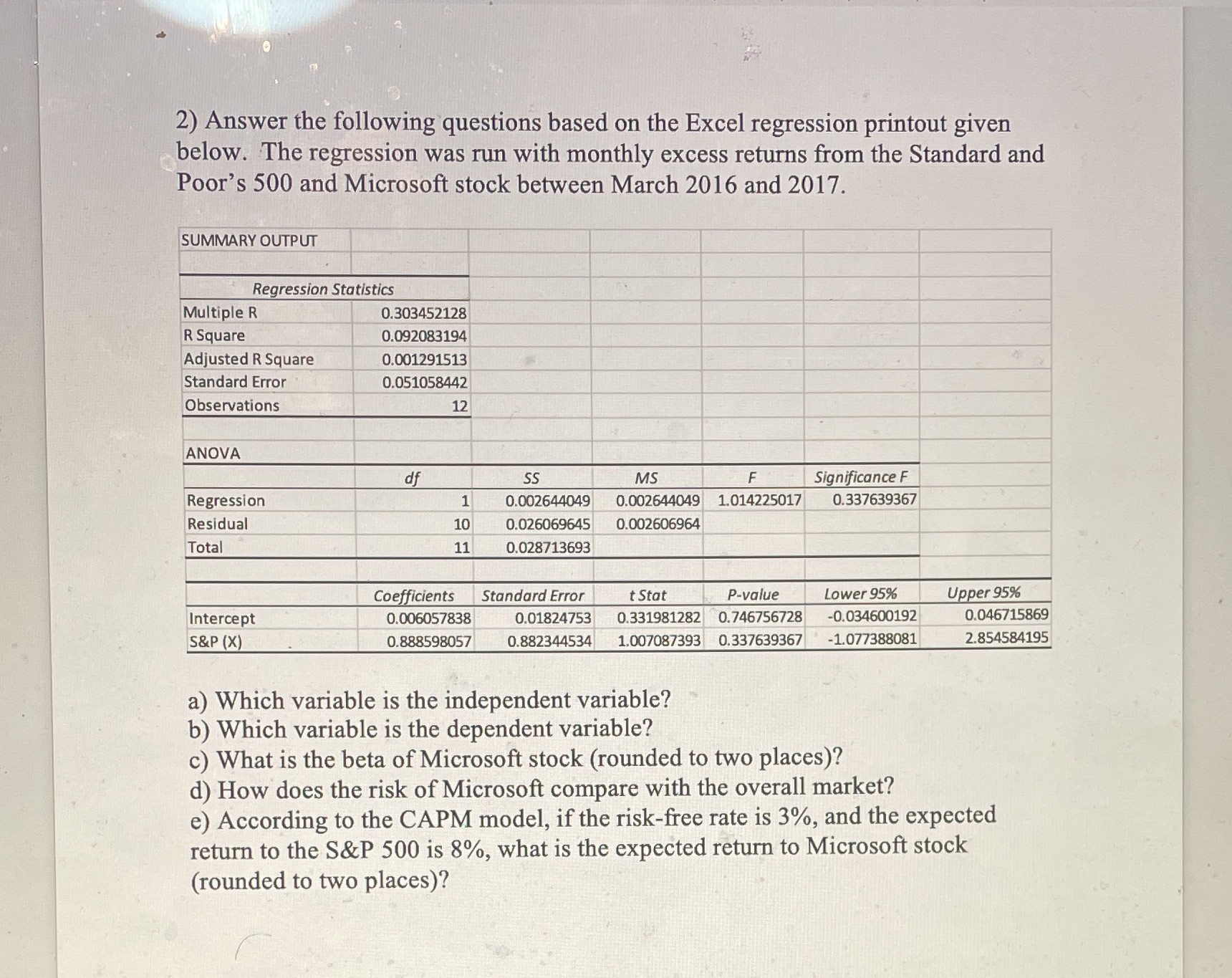

Question: 2) Answer the following questions based on the Excel regression printout given below. The regression was run with monthly excess returns from the Standard and

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock