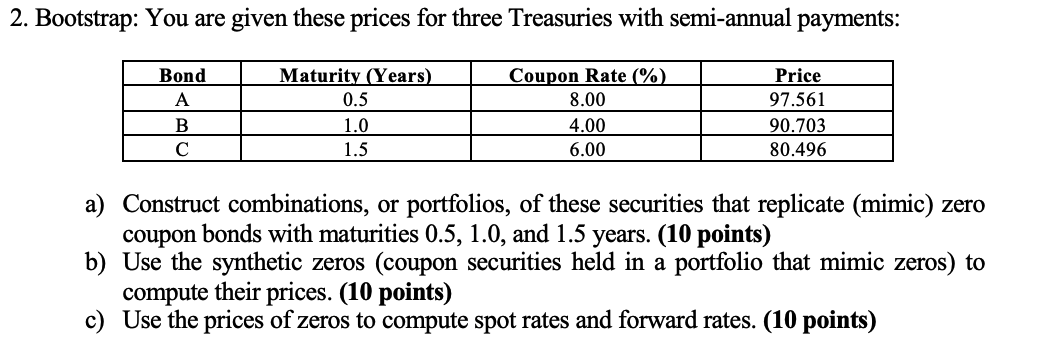

Question: 2. Bootstrap: You are given these prices for three Treasuries with semi-annual payments: Bond A B C Maturity (Years) 0.5 1.0 1.5 Coupon Rate

2. Bootstrap: You are given these prices for three Treasuries with semi-annual payments: Bond A B C Maturity (Years) 0.5 1.0 1.5 Coupon Rate (%) 8.00 4.00 6.00 Price 97.561 90.703 80.496 a) Construct combinations, or portfolios, of these securities that replicate (mimic) zero coupon bonds with maturities 0.5, 1.0, and 1.5 years. (10 points) b) Use the synthetic zeros (coupon securities held in a portfolio that mimic zeros) to compute their prices. (10 points) c) Use the prices of zeros to compute spot rates and forward rates. (10 points)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock