Question: (2) Consider a trinomial tree model with A(0) = 10, risk-free interest rate r = 0.1, S(0) = 100 and independent one-period returns 0.2 in

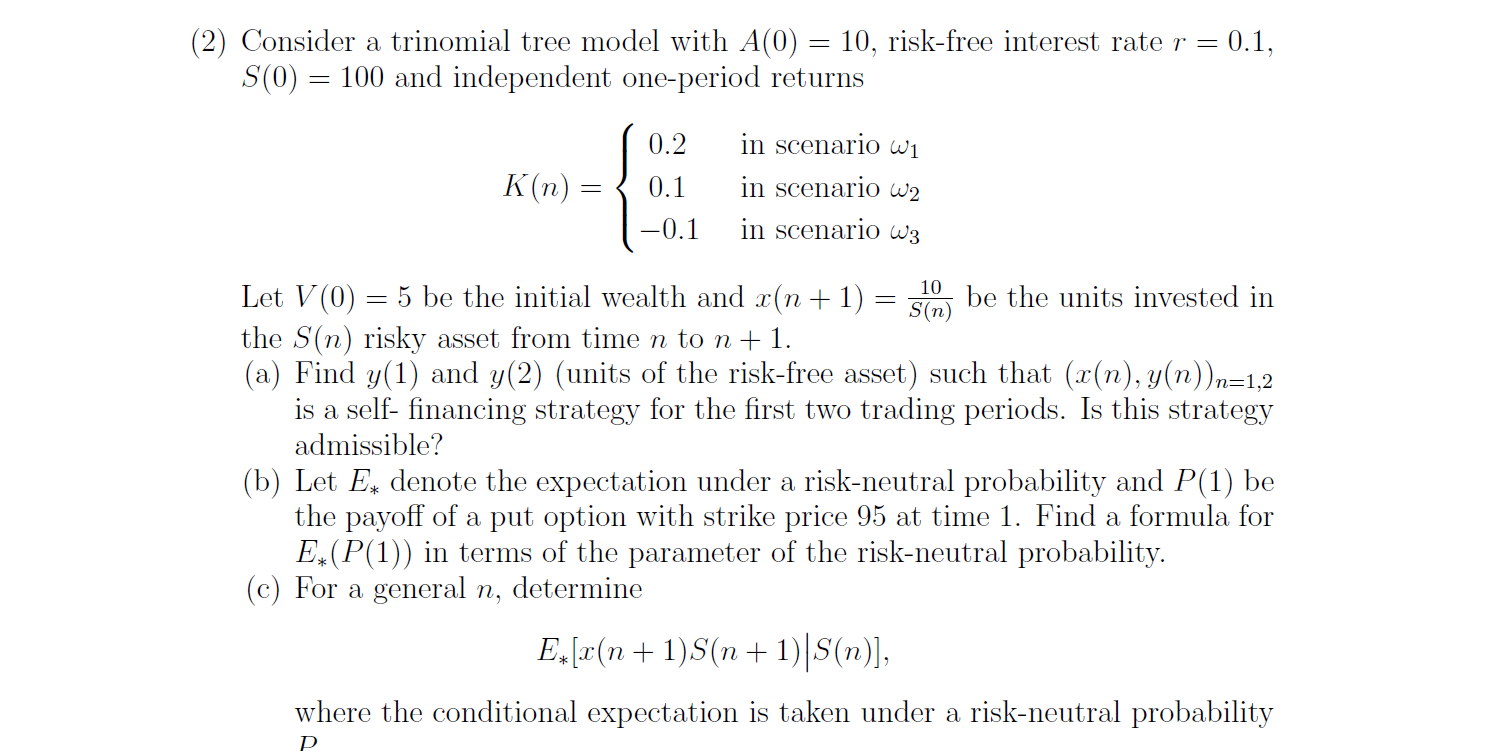

(2) Consider a trinomial tree model with A(0) = 10, risk-free interest rate r = 0.1, S(0) = 100 and independent one-period returns 0.2 in scenario K(n) = 0.1 in scenario 2 -0.1 in scenario 3 Let V(0) = 5 be the initial wealth and x(n+1) 10 S(n) be the units invested in the S(n) risky asset from time n to n + 1. (a) Find y(1) and y(2) (units of the risk-free asset) such that (x(n), y(n))n=1,2 is a self- financing strategy for the first two trading periods. Is this strategy admissible? (b) Let E, denote the expectation under a risk-neutral probability and P(1) be the payoff of a put option with strike price 95 at time 1. Find a formula for E (P(1)) in terms of the parameter of the risk-neutral probability. (c) For a general n, determine E.[x(n+1) S(n+1) S(n)], where the conditional expectation is taken under a risk-neutral probability P (2) Consider a trinomial tree model with A(0) = 10, risk-free interest rate r = 0.1, S(0) = 100 and independent one-period returns 0.2 in scenario K(n) = 0.1 in scenario 2 -0.1 in scenario 3 Let V(0) = 5 be the initial wealth and x(n+1) 10 S(n) be the units invested in the S(n) risky asset from time n to n + 1. (a) Find y(1) and y(2) (units of the risk-free asset) such that (x(n), y(n))n=1,2 is a self- financing strategy for the first two trading periods. Is this strategy admissible? (b) Let E, denote the expectation under a risk-neutral probability and P(1) be the payoff of a put option with strike price 95 at time 1. Find a formula for E (P(1)) in terms of the parameter of the risk-neutral probability. (c) For a general n, determine E.[x(n+1) S(n+1) S(n)], where the conditional expectation is taken under a risk-neutral probability P

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts