Question: 2) Consider the following investor utility function U = E(1) - (A/2)02 where U is the investor's utility, E() is a portfolio's expected return, A

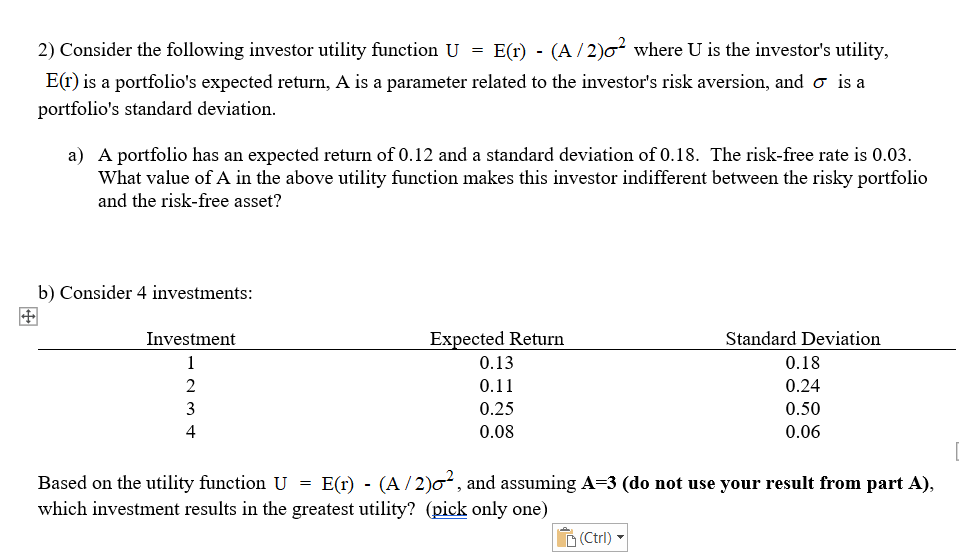

2) Consider the following investor utility function U = E(1) - (A/2)02 where U is the investor's utility, E() is a portfolio's expected return, A is a parameter related to the investor's risk aversion, and o is a portfolio's standard deviation. a) A portfolio has an expected return of 0.12 and a standard deviation of 0.18. The risk-free rate is 0.03. What value of A in the above utility function makes this investor indifferent between the risky portfolio and the risk-free asset? b) Consider 4 investments: Investment 1 2 3 4 Expected Return 0.13 0.11 0.25 0.08 Standard Deviation 0.18 0.24 0.50 0.06 Based on the utility function U = E(r) - (A/2)0?, and assuming A=3 (do not use your result from part A), which investment results in the greatest utility? (pick only one) (Ctrl)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts