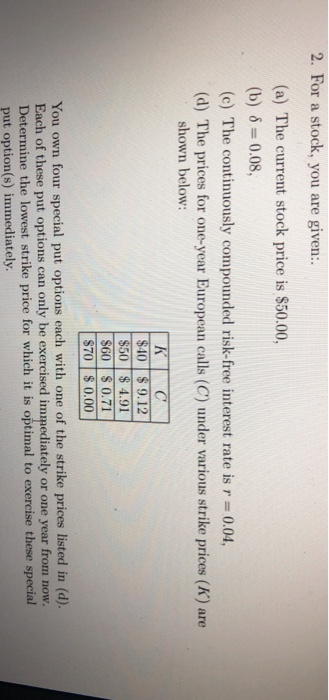

Question: 2. For a stock, you are given:. (a) The current stock price is $50.00, (b) 8 = 0.08 (c) The continuously compounded risk-free interest rate

2. For a stock, you are given:. (a) The current stock price is $50.00, (b) 8 = 0.08 (c) The continuously compounded risk-free interest rate is r = 0.04, (d) The prices for one-year European calls (C) under various strike prices (R) are shown below: K $40 $ 9.12 $50 $ 4.91 $60 $ 0.71 $70 $ 0.00 You own four special put options each with one of the strike prices listed in (d). Each of these put options can only be exercised immediately or one year from now. Determine the lowest strike price for which it is optimal to exercise these special put option(s) immediately. 2. For a stock, you are given:. (a) The current stock price is $50.00, (b) 8 = 0.08 (c) The continuously compounded risk-free interest rate is r = 0.04, (d) The prices for one-year European calls (C) under various strike prices (R) are shown below: K $40 $ 9.12 $50 $ 4.91 $60 $ 0.71 $70 $ 0.00 You own four special put options each with one of the strike prices listed in (d). Each of these put options can only be exercised immediately or one year from now. Determine the lowest strike price for which it is optimal to exercise these special put option(s) immediately

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts