Question: 2 . Information about Bonds ( A ) and ( B ) is given below. Construct a portfolio of these two

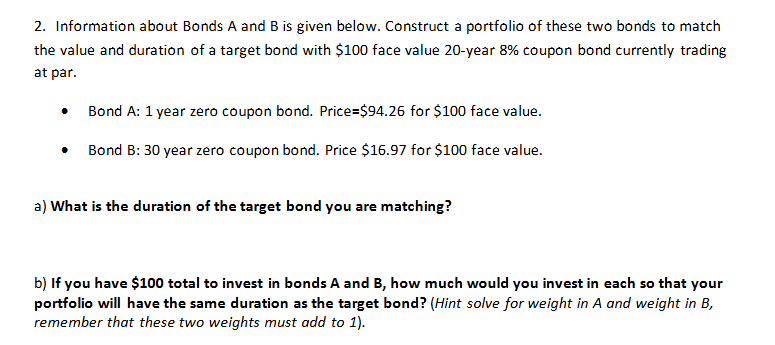

Information about Bonds A and B is given below. Construct a portfolio of these two bonds to match the value and duration of a target bond with $ face value year coupon bond currently trading at par. Bond A: year zero coupon bond. Price $ for $ face value. Bond B: year zero coupon bond. Price $ for $ face value. a What is the duration of the target bond you are matching? b If you have mathbf$ total to invest in bonds mathbfA and B how much would you invest in each so that your portfolio will have the same duration as the target bond? Hint solve for weight in A and weight in B remember that these two weights must add to

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock