Question: 2. Let W be a Brownian motion and R be an It process satisfying the stochastic differential equation dR = (8-2R+) dt +5dWt, R

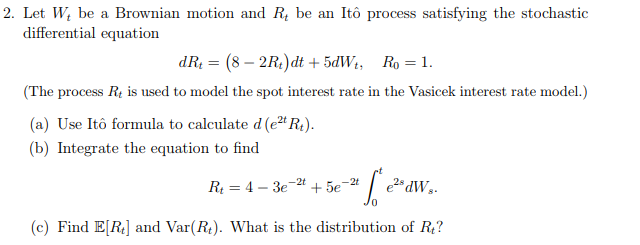

2. Let W be a Brownian motion and R be an It process satisfying the stochastic differential equation dR = (8-2R+) dt +5dWt, R = 1. (The process Rt is used to model the spot interest rate in the Vasicek interest rate model.) (a) Use It formula to calculate d (et Rt). (b) Integrate the equation to find Rt 4-3e2+5e- -2t esdWs- (c) Find E[R] and Var(R). What is the distribution of R?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock