Question: 2 points What is the market beta estimated using the three-factor model? Type your answer... 2 points What is the size beta estimated using the

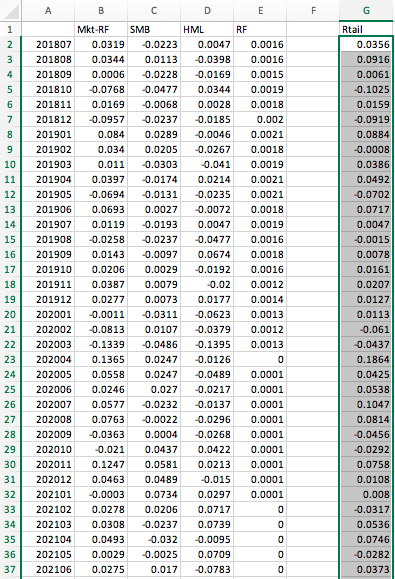

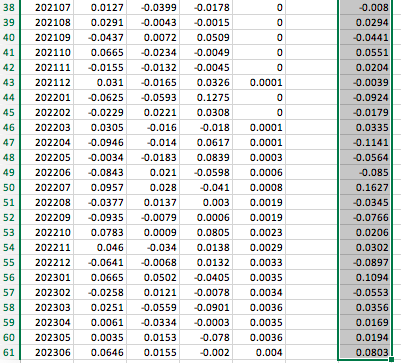

2 points What is the market beta estimated using the three-factor model? Type your answer... 2 points What is the size beta estimated using the three-factor model? Type your answer... 2 points What is the value beta estimated using the three-factor model? Type your answer... 2 points What is the adjusted R-squared for the three-factor model? Type your answer... 2 points Which of the coefficients appear significant in the three-factor model? Select all that apply. coefficient on the market factor coefficient on the value factor coefficient on the size factor intercept 2 points Does the three-factor model explain the returns on the retail portfolio better than the single-factor CAPM model? If so, which statistic serves as the evidence? Yes; Adjusted R-squared. Yes; the t-statistics on the market factor. Yes; the t-statistics on the value factor. No 2 points To prevent error carried forwards, assume that the coefficient on the HML is -0.5 , and it is statistically significant. Based on this information, the retail portfolio exhibits the highest exposure to which category of stocks? Small stocks Large stocks Value stocks Growth stocks Using the Regression tool in the Excel Data Analysis pack, run a CAPM model regression of the retail portfolio. CAPM requires just a single factor, the excess return on the market, as the independent variable. What is the beta of the retail portfolio? Type your answer... 2 points What is the t-statistics for the estimated beta? 2 points What is the market beta estimated using the three-factor model? Type your answer... 2 points What is the size beta estimated using the three-factor model? Type your answer... 2 points What is the value beta estimated using the three-factor model? Type your answer... 2 points What is the adjusted R-squared for the three-factor model? Type your answer... 2 points Which of the coefficients appear significant in the three-factor model? Select all that apply. coefficient on the market factor coefficient on the value factor coefficient on the size factor intercept 2 points Does the three-factor model explain the returns on the retail portfolio better than the single-factor CAPM model? If so, which statistic serves as the evidence? Yes; Adjusted R-squared. Yes; the t-statistics on the market factor. Yes; the t-statistics on the value factor. No 2 points To prevent error carried forwards, assume that the coefficient on the HML is -0.5 , and it is statistically significant. Based on this information, the retail portfolio exhibits the highest exposure to which category of stocks? Small stocks Large stocks Value stocks Growth stocks Using the Regression tool in the Excel Data Analysis pack, run a CAPM model regression of the retail portfolio. CAPM requires just a single factor, the excess return on the market, as the independent variable. What is the beta of the retail portfolio? Type your answer... 2 points What is the t-statistics for the estimated beta

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts