Question: 2. (Portfolio Construction with Different Objectives) Tab Portfolio Selection in the file hw1.xlsx contains the following data for the returns of five (5) assets

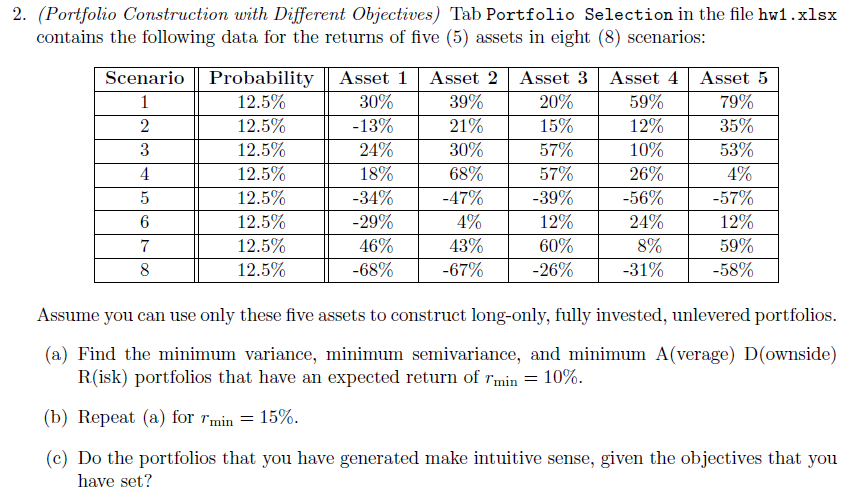

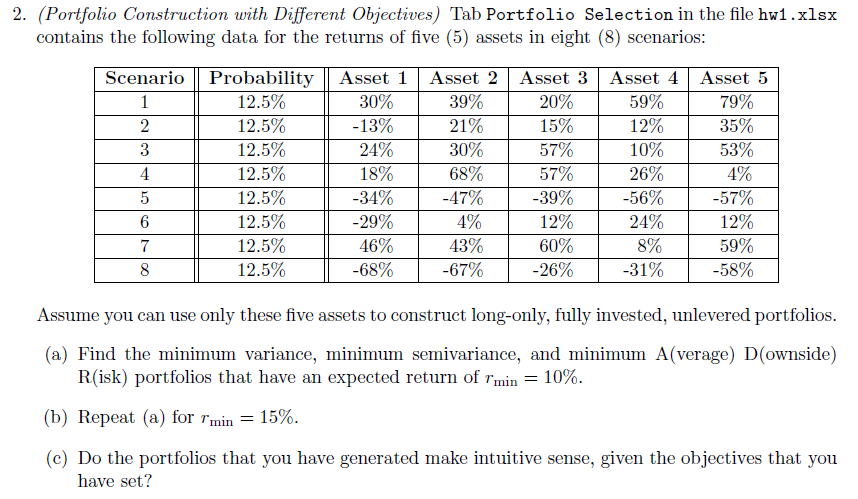

2. (Portfolio Construction with Different Objectives) Tab Portfolio Selection in the file hw1.xlsx contains the following data for the returns of five (5) assets in eight (8) scenarios: Scenario Probability Asset 1 Asset 2 Asset 3 Asset 4 Asset 5 1 12.5% 30% 39% 20% 59% 79% 2 12.5% -13% 21% 15% 12% 35% 3 12.5% 24% 30% 57% 10% 53% 4 12.5% 18% 68% 57% 26% 4% 5 12.5% -34% -47% -39% -56% -57% 6 12.5% -29% 4% 12% 24% 12% 7 12.5% 46% 43% 60% 8% 59% 8 12.5% -68% -67% -26% -31% -58% Assume you can use only these five assets to construct long-only, fully invested, unlevered portfolios. (a) Find the minimum variance, minimum semivariance, and minimum A(verage) D(ownside) R(isk) portfolios that have an expected return of "min = 10%. (b) Repeat (a) for min = 15%. (c) Do the portfolios that you have generated make intuitive sense, given the objectives that you have set?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts