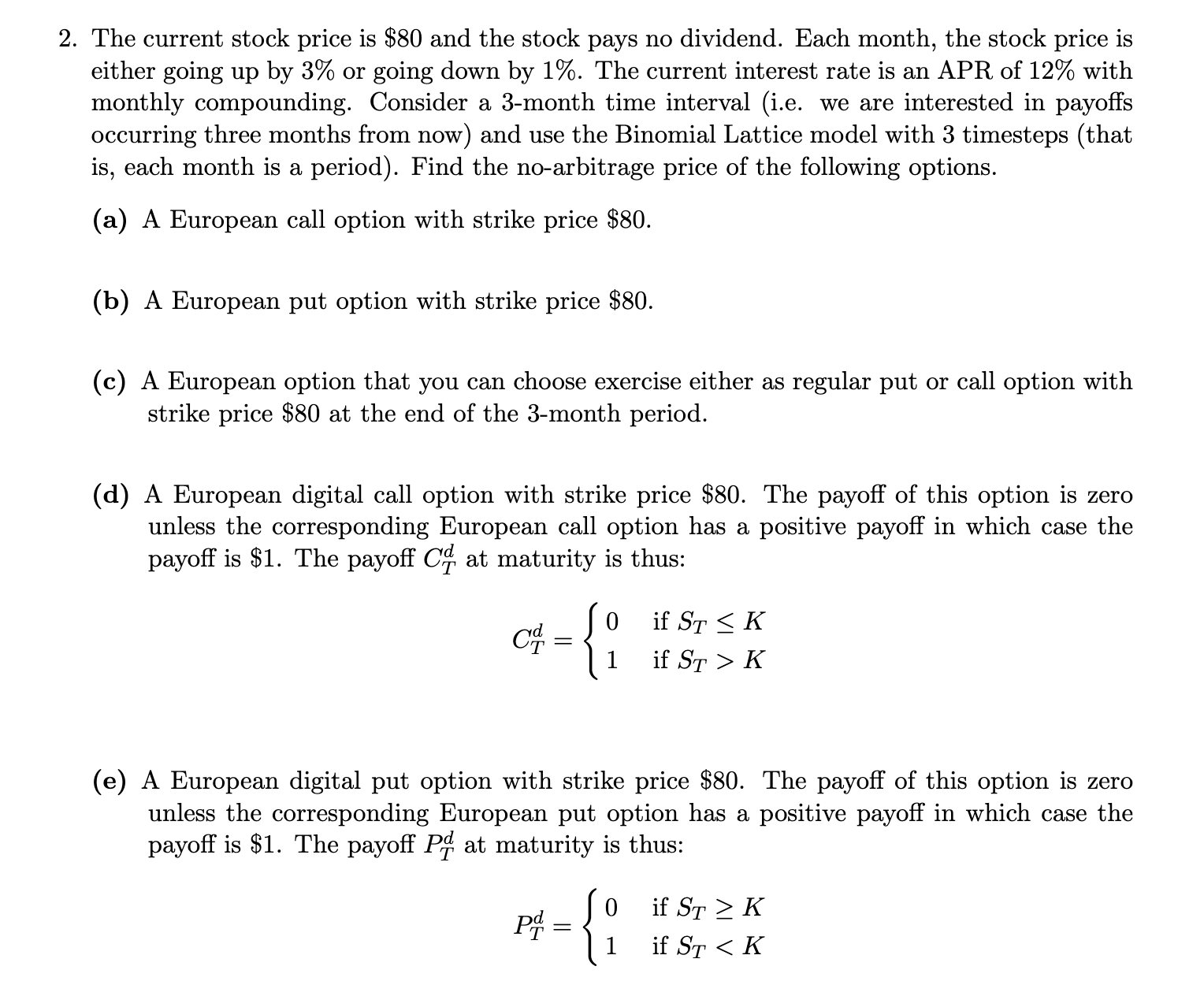

2. The current stock price is $80 and the stock pays no dividend. Each month, the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Binomial Option Pricing with NoArbitrage Given Current Stock Price S 80 Upward Price Movement u 103 ... View the full answer

Related Book For

Posted Date: