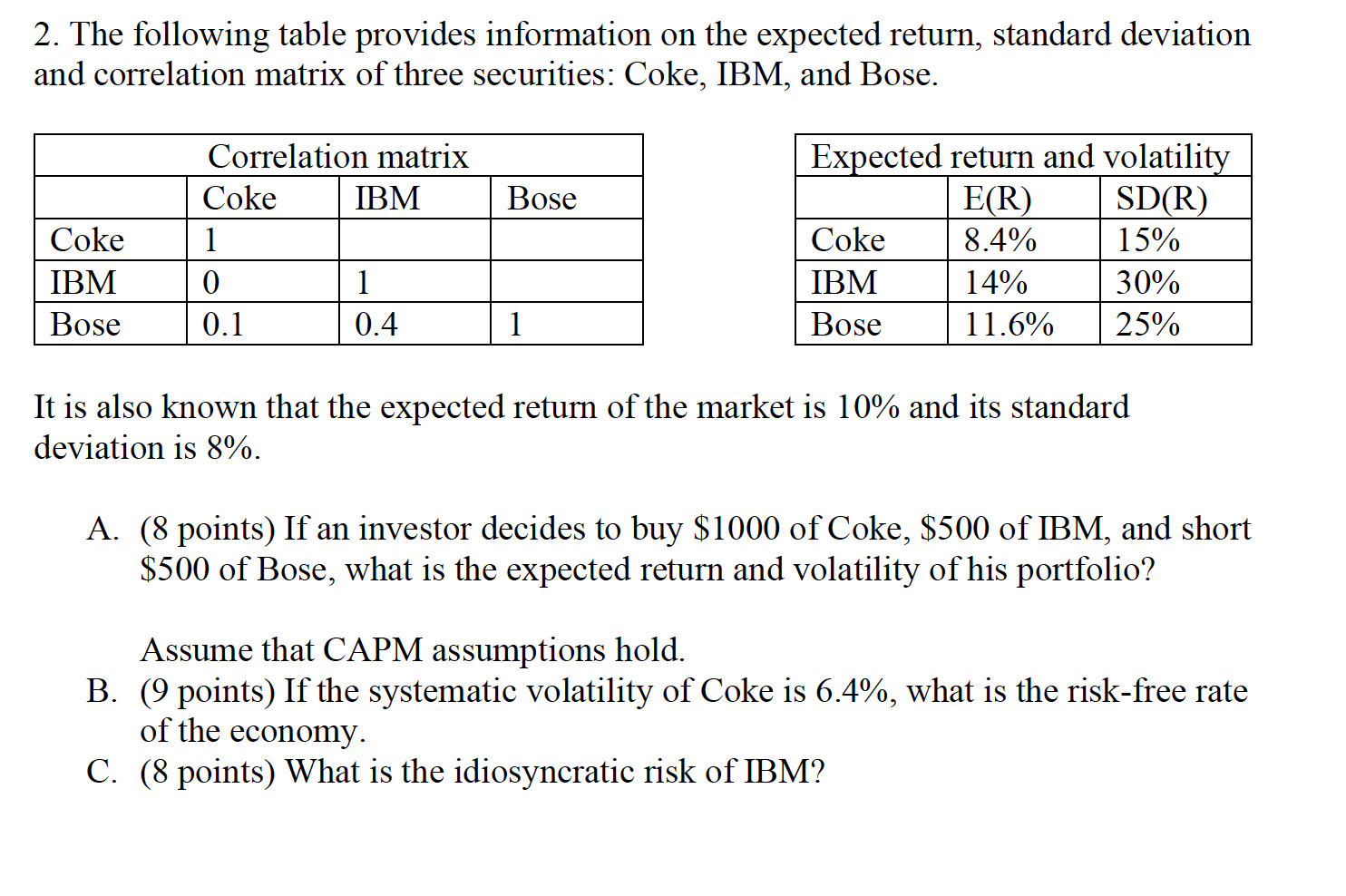

Question: 2. The following table provides information on the expected return, standard deviation and correlation matrix of three securities: Coke, IBM, and Bose. Bose Coke IBM

2. The following table provides information on the expected return, standard deviation and correlation matrix of three securities: Coke, IBM, and Bose. Bose Coke IBM Bose Correlation matrix Coke IBM 1 0 1 0.1 0.4 Expected return and volatility E(R) SD(R) Coke 8.4% 15% IBM 14% 30% Bose 11.6% 25% 1 It is also known that the expected return of the market is 10% and its standard deviation is 8%. A. (8 points) If an investor decides to buy $1000 of Coke, $500 of IBM, and short $500 of Bose, what is the expected return and volatility of his portfolio? Assume that CAPM assumptions hold. B. (9 points) If the systematic volatility of Coke is 6.4%, what is the risk-free rate of the economy. C. (8 points) What is the idiosyncratic risk of IBM

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts