Question: (20 points) As seen at time To (today), the forward annual discount factors (trivially including P(To, T1)) are known to be P(T., T1) = 0.950,

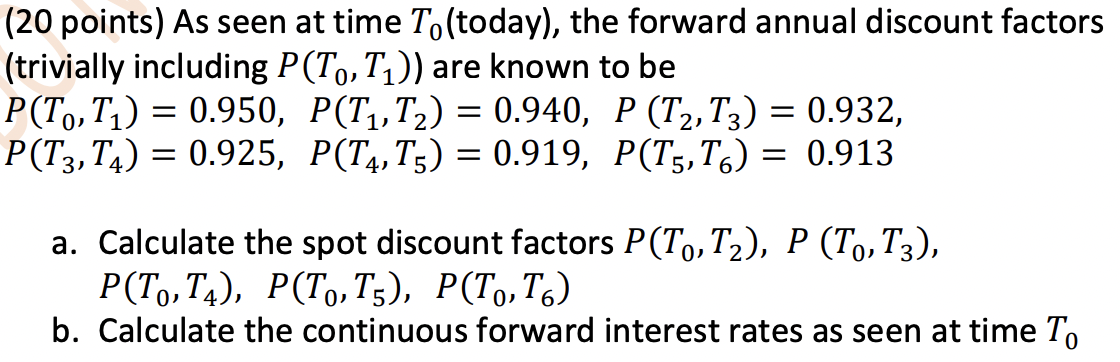

(20 points) As seen at time To (today), the forward annual discount factors (trivially including P(To, T1)) are known to be P(T., T1) = 0.950, P(T1,72) = 0.940, P (T2,73) = 0.932, P(T3,T4) = 0.925, P(T4,T3) = 0.919, P(T5, T6) = 0.913 a. Calculate the spot discount factors P(T,,T2), P (To, T3), P(T,,T4), P(T., T3), P(T,,T) b. Calculate the continuous forward interest rates as seen at time To

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock