Question: 27. Continuing from previous question, use Modified Duration and Convexity to approximate the percentage change in price of the bond when its market rate change

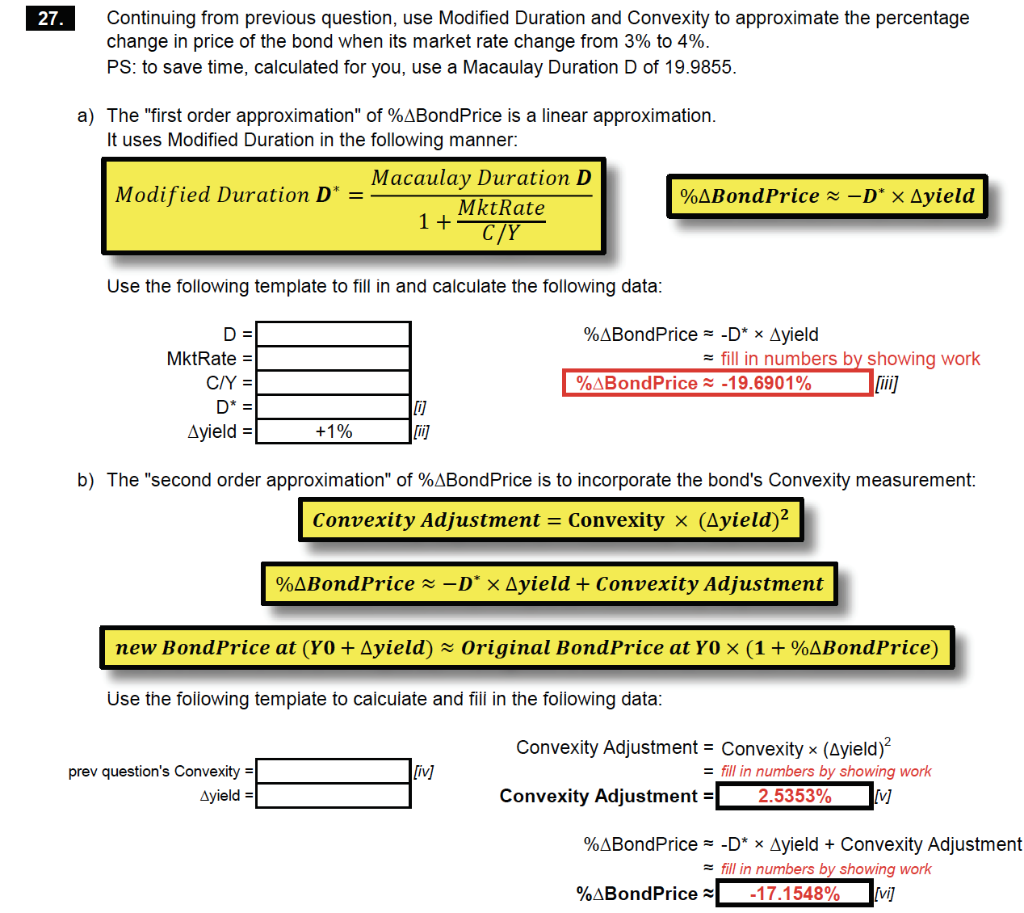

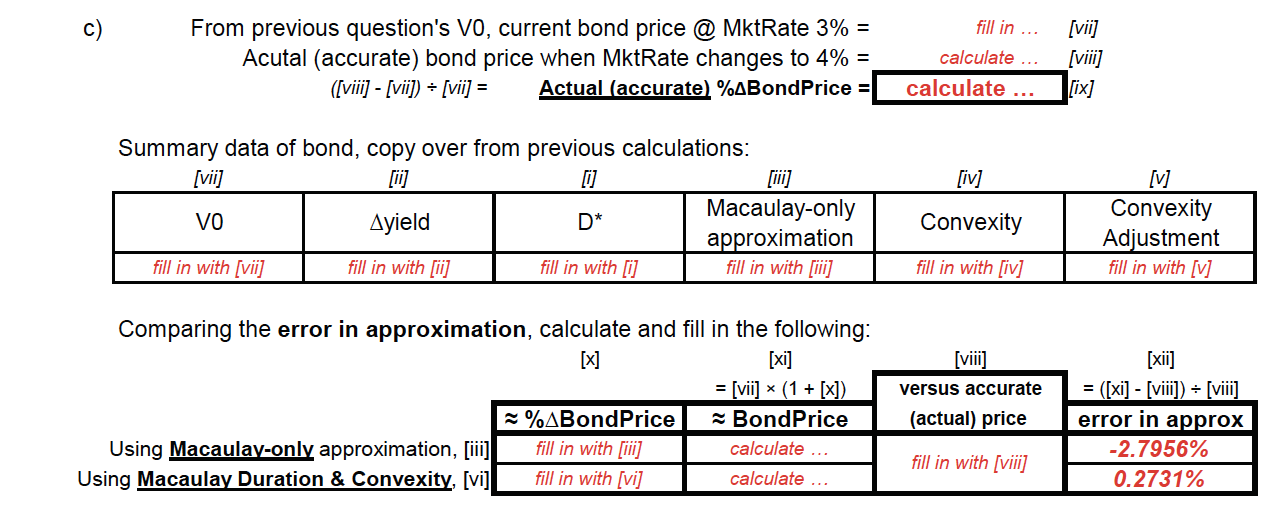

27. Continuing from previous question, use Modified Duration and Convexity to approximate the percentage change in price of the bond when its market rate change from 3% to 4%. PS: to save time, calculated for you, use a Macaulay Duration D of 19.9855. a) The "first order approximation" of %ABondPrice is a linear approximation. It uses Modified Duration in the following manner: %ABondPrice z-D* x Ayield Macaulay Duration D Modified Duration D* = MktRate 1 + C/Y Use the following template to fill in and calculate the following data: D = %ABondPrice = -D* * Ayield = fill in numbers by showing work %ABondPrice -19.6901% MktRate = C/Y = D* = Ayield = [ +1% b) The "second order approximation" of %ABondPrice is to incorporate the bond's Convexity measurement: Convexity Adjustment = Convexity x (Ayield)2 %ABondPrice 2 -D* x Ayield + Convexity Adjustment new BondPrice at (YO + Ayield) Original BondPrice at Yo x (1 + %ABondPrice) Use the following template to calculate and fill in the following data: [iv] prev question's Convexity = Ayield Convexity Adjustment = Convexity * (Ayield)? = fill in numbers by showing work Convexity Adjustment = 2.5353% [v] %ABondPrice = -D* * Ayield + Convexity Adjustment = fill in numbers by showing work %ABondPrice -17.1548% [vi] c c) fill in ... From previous question's VO, current bond price @ MktRate 3% = Acutal (accurate) bond price when MktRate changes to 4% = ([viii] - [vii) = [vii] = Actual (accurate %ABondPrice = calculate [vii] [viii] [ix] calculate ... [iv] Summary data of bond, copy over from previous calculations: [vii] Macaulay-only VO Ayield D* approximation fill in with [vii] fill in with [ii] fill in with [i] fill in with [iii] Convexity [v] Convexity Adjustment fill in with [v] fill in with [iv] [vii] versus accurate Comparing the error in approximation, calculate and fill in the following: [x] [xi] = [vii] * (1 + [x]) %ABondPrice BondPrice Using Macaulay-only approximation, [ii] fill in with [ii] calculate ... Using Macaulay Duration & Convexity, [vi] fill in with [vi] calculate ... [xii] = ([xi] - [viii]) = [viii] error in approx -2.7956% (actual) price fill in with [viii] 0.2731% 27. Continuing from previous question, use Modified Duration and Convexity to approximate the percentage change in price of the bond when its market rate change from 3% to 4%. PS: to save time, calculated for you, use a Macaulay Duration D of 19.9855. a) The "first order approximation" of %ABondPrice is a linear approximation. It uses Modified Duration in the following manner: %ABondPrice z-D* x Ayield Macaulay Duration D Modified Duration D* = MktRate 1 + C/Y Use the following template to fill in and calculate the following data: D = %ABondPrice = -D* * Ayield = fill in numbers by showing work %ABondPrice -19.6901% MktRate = C/Y = D* = Ayield = [ +1% b) The "second order approximation" of %ABondPrice is to incorporate the bond's Convexity measurement: Convexity Adjustment = Convexity x (Ayield)2 %ABondPrice 2 -D* x Ayield + Convexity Adjustment new BondPrice at (YO + Ayield) Original BondPrice at Yo x (1 + %ABondPrice) Use the following template to calculate and fill in the following data: [iv] prev question's Convexity = Ayield Convexity Adjustment = Convexity * (Ayield)? = fill in numbers by showing work Convexity Adjustment = 2.5353% [v] %ABondPrice = -D* * Ayield + Convexity Adjustment = fill in numbers by showing work %ABondPrice -17.1548% [vi] c c) fill in ... From previous question's VO, current bond price @ MktRate 3% = Acutal (accurate) bond price when MktRate changes to 4% = ([viii] - [vii) = [vii] = Actual (accurate %ABondPrice = calculate [vii] [viii] [ix] calculate ... [iv] Summary data of bond, copy over from previous calculations: [vii] Macaulay-only VO Ayield D* approximation fill in with [vii] fill in with [ii] fill in with [i] fill in with [iii] Convexity [v] Convexity Adjustment fill in with [v] fill in with [iv] [vii] versus accurate Comparing the error in approximation, calculate and fill in the following: [x] [xi] = [vii] * (1 + [x]) %ABondPrice BondPrice Using Macaulay-only approximation, [ii] fill in with [ii] calculate ... Using Macaulay Duration & Convexity, [vi] fill in with [vi] calculate ... [xii] = ([xi] - [viii]) = [viii] error in approx -2.7956% (actual) price fill in with [viii] 0.2731%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts