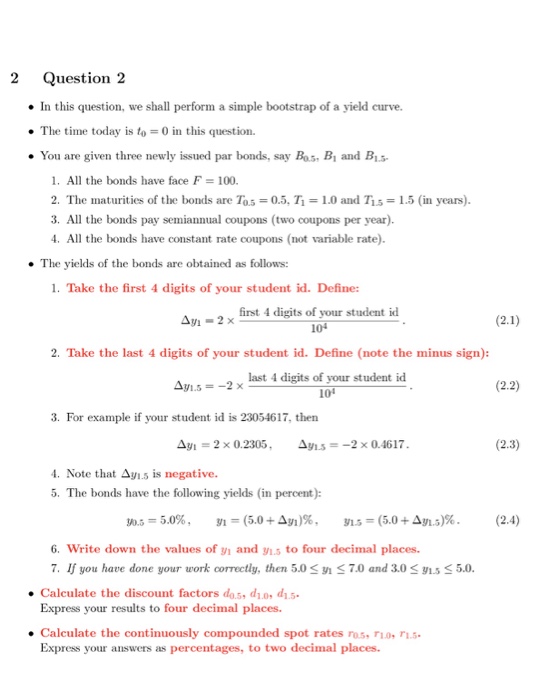

Question: 2Question 2 In this question, we shall perform a simple bootstrap of a yield curve. The time today is to = 0 in this question.

2Question 2 In this question, we shall perform a simple bootstrap of a yield curve. The time today is to = 0 in this question. . You are given three newly issued par bonds, say Bo.s. Bi and Bi 1. All the bonds have face F 100 2. The maturities of the bonds are Tas = 0.5, T1 = 1.0 and T1.5 = 1.5 (in years). 3. All the bonds pay semiannual coupons (two coupons per year). . All the bonds have constant rate coupons (not variable rate). . The yields of the bonds are obtained as follows: 1. Take the first 4 digits of your student id. Define: first 4 digits of your student id 104 2. Take the last 4 digits of your student id. Define (note the minus sign): last 4 digits of your student id 104 (2.2) 3. For example if your student id is 23054617, then (2.3) 4. Note that 1.5 is negative. 5. The bonds have the following yields (in percent): (2.4) 6. Write down the values of h and ys to four decimal places. 7 you have done your work comectly, then 5.0 y1 7,0 and 3.0 y1.5 5.0. Calculate the discount factors dos, d.o dis. Express your results to four decimal places. Calculate the continuously compounded spot rates ras, r1.0, r1.5. Express your answers as percentages, to two decimal places

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts