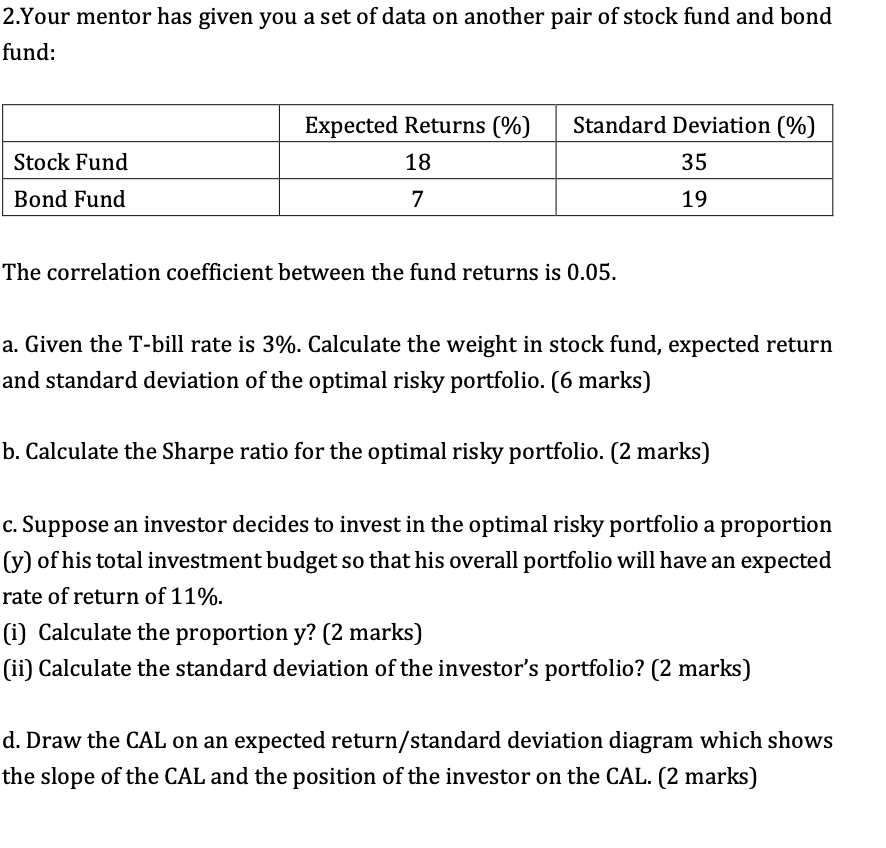

Question: 2.Your mentor has given you a set of data on another pair of stock fund and bond fund: The correlation coefficient between the fund returns

2.Your mentor has given you a set of data on another pair of stock fund and bond fund: The correlation coefficient between the fund returns is 0.05. a. Given the T-bill rate is 3%. Calculate the weight in stock fund, expected return and standard deviation of the optimal risky portfolio. ( 6 marks) b. Calculate the Sharpe ratio for the optimal risky portfolio. (2 marks) c. Suppose an investor decides to invest in the optimal risky portfolio a proportion (y) of his total investment budget so that his overall portfolio will have an expected rate of return of 11% (i) Calculate the proportion y? (2 marks) (ii) Calculate the standard deviation of the investor's portfolio? ( 2 marks) d. Draw the CAL on an expected return/standard deviation diagram which shows the slope of the CAL and the position of the investor on the CAL. (2 marks) 2.Your mentor has given you a set of data on another pair of stock fund and bond fund: The correlation coefficient between the fund returns is 0.05. a. Given the T-bill rate is 3%. Calculate the weight in stock fund, expected return and standard deviation of the optimal risky portfolio. ( 6 marks) b. Calculate the Sharpe ratio for the optimal risky portfolio. (2 marks) c. Suppose an investor decides to invest in the optimal risky portfolio a proportion (y) of his total investment budget so that his overall portfolio will have an expected rate of return of 11% (i) Calculate the proportion y? (2 marks) (ii) Calculate the standard deviation of the investor's portfolio? ( 2 marks) d. Draw the CAL on an expected return/standard deviation diagram which shows the slope of the CAL and the position of the investor on the CAL. (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts