Question: 3. 1 (10 pts) Consider 3 securities with expected returns, standard deviations of returns and correlations between returns given below = = M1 = 0.2

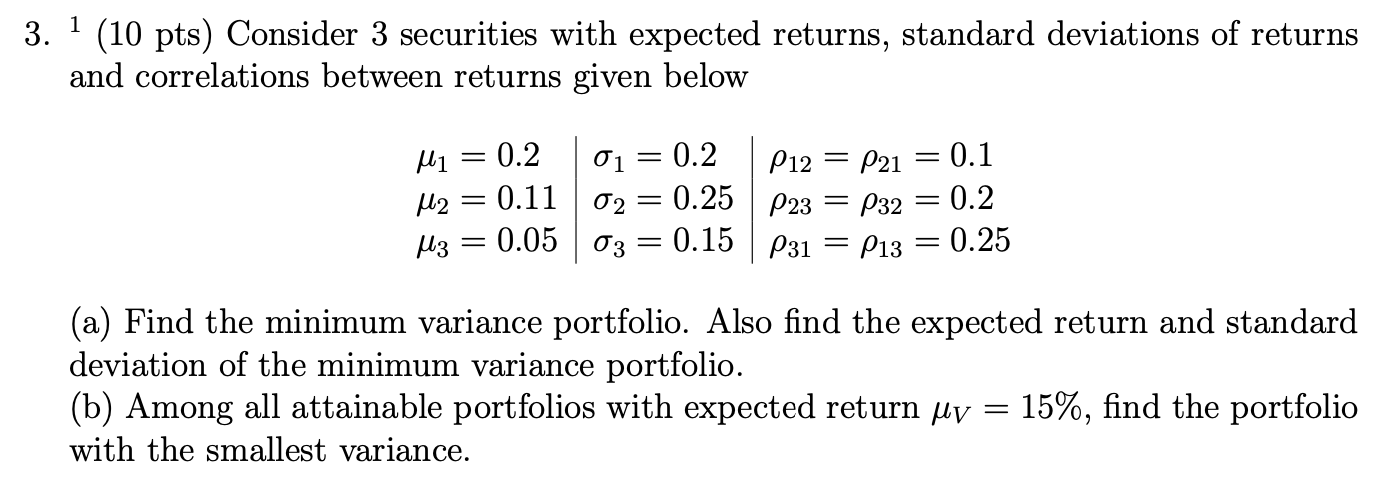

3. 1 (10 pts) Consider 3 securities with expected returns, standard deviations of returns and correlations between returns given below = = M1 = 0.2 M2 = 0.11 M3 = 0.05 = 01 = 0.2 P12 = P21 = 0.1 02 = = 0.25 P23 P32 = 0.2 03 = 0.15 P31 EP13 = 0.25 (a) Find the minimum variance portfolio. Also find the expected return and standard deviation of the minimum variance portfolio. (b) Among all attainable portfolios with expected return iv 15%, find the portfolio with the smallest variance. = 3. 1 (10 pts) Consider 3 securities with expected returns, standard deviations of returns and correlations between returns given below = = M1 = 0.2 M2 = 0.11 M3 = 0.05 = 01 = 0.2 P12 = P21 = 0.1 02 = = 0.25 P23 P32 = 0.2 03 = 0.15 P31 EP13 = 0.25 (a) Find the minimum variance portfolio. Also find the expected return and standard deviation of the minimum variance portfolio. (b) Among all attainable portfolios with expected return iv 15%, find the portfolio with the smallest variance. =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts