Question: 3. [20pts] This problem is an estimation and hypothesis testing exercise using the Law of Large Numbers (LLN) and Central Limit Theorem (CLT). As we

![3. [20pts] This problem is an estimation and hypothesis testing exercise](https://s3.amazonaws.com/si.experts.images/answers/2024/06/667e3fbbb816e_883667e3fbba31a2.jpg)

![2 0] Annual Returns on BioStar (BS): Year Return 2017 - 0.08](https://s3.amazonaws.com/si.experts.images/answers/2024/06/667e3fbda5e66_885667e3fbd99126.jpg)

![2018 - 0.05 2019 + 0.10 2020 + 0.15 (3-a) [3pts] To](https://s3.amazonaws.com/si.experts.images/answers/2024/06/667e3fbdd9fa3_885667e3fbdcb33a.jpg)

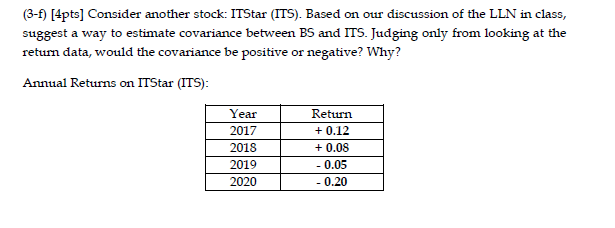

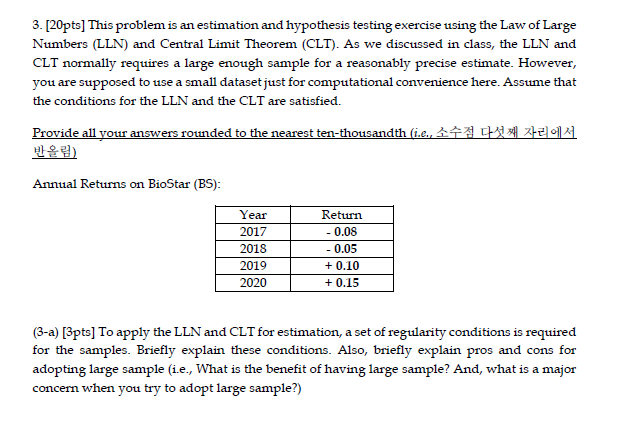

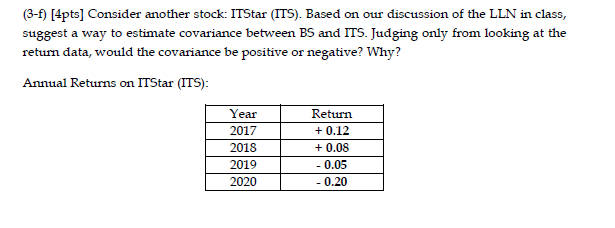

3. [20pts] This problem is an estimation and hypothesis testing exercise using the Law of Large Numbers (LLN) and Central Limit Theorem (CLT). As we discussed in class, the LLN and CLT normally requires a large enough sample for a reasonably precise estimate. However, you are supposed to use a small dataset just for computational convenience here. Assume that the conditions for the LLN and the CLT are satisfied. Provide all your answers rounded to the nearest ten-thousandth (ic., 1 7 1 2 2 0] Annual Returns on BioStar (BS): Year Return 2017 - 0.08 2018 - 0.05 2019 + 0.10 2020 + 0.15 (3-a) [3pts] To apply the LLN and CLT for estimation, a set of regularity conditions is required for the samples. Briefly explain these conditions. Also, briefly explain pros and cons for adopting large sample (i.e., What is the benefit of having large sample? And, what is a major concern when you try to adopt large sample?)(3-d) [4pts] Show 95% confidence interval for the true expected return () of BS. Even though we have very small sample, assume that the t-stat follows not a Student t-distribution but a normal distribution.(3-e) [4pts] Test the following hypothesis at the significance level of 5%. Hoi Has = 0(3-f) [4pts] Consider another stock: ITStar (ITS). Based on our discussion of the LLN in class, suggest a way to estimate covariance between BS and ITS. Judging only from looking at the return data, would the covariance be positive or negative? Why? Annual Returns on ITStar (ITS): Year Return 2017 + 0.12 2018 + 0.08 2019 - 0.05 2020 - 0.20

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts