Question: 3. Based on the information given in the table, answer the following questions Market Portfolio 0.12 0.2 Risk-free asset 0.02 Stock XStock YStockZ 0.18 0.3

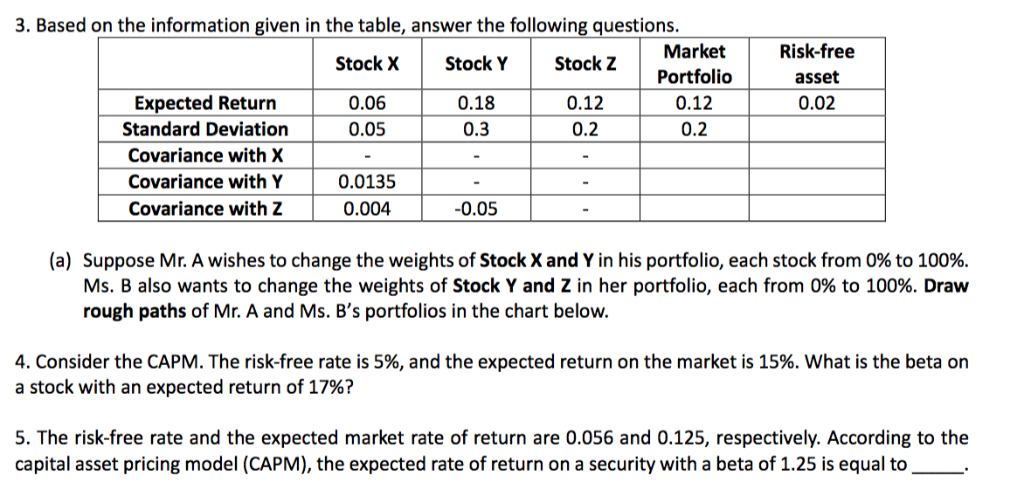

3. Based on the information given in the table, answer the following questions Market Portfolio 0.12 0.2 Risk-free asset 0.02 Stock XStock YStockZ 0.18 0.3 0.06 0.05 0.12 0.2 Expected Return Standard Deviation Covariance with X Covariance with Y Covariance with Z 0.0135 0.004 0.05 (a) Suppose Mr. A wishes to change the weights of Stock X and Y in his portfolio, each stock from 0% to 100%. Ms. B also wants to change the weights of Stock Y and Z in her portfolio, each from 0% to 100%. Draw rough paths of Mr. A and Ms. B's portfolios in the chart below. 4. Consider the CAPM. The risk-free rate is 5%, and the expected return on the market is 15%, what is the beta on a stock with an expected return of 17%? 5. The risk-free rate and the expected market rate of return are 0.056 and 0.125, respectively. According to the capital asset pricing model (CAPM), the expected rate of return on a security with a beta of 1.25 is equal to 3. Based on the information given in the table, answer the following questions Market Portfolio 0.12 0.2 Risk-free asset 0.02 Stock XStock YStockZ 0.18 0.3 0.06 0.05 0.12 0.2 Expected Return Standard Deviation Covariance with X Covariance with Y Covariance with Z 0.0135 0.004 0.05 (a) Suppose Mr. A wishes to change the weights of Stock X and Y in his portfolio, each stock from 0% to 100%. Ms. B also wants to change the weights of Stock Y and Z in her portfolio, each from 0% to 100%. Draw rough paths of Mr. A and Ms. B's portfolios in the chart below. 4. Consider the CAPM. The risk-free rate is 5%, and the expected return on the market is 15%, what is the beta on a stock with an expected return of 17%? 5. The risk-free rate and the expected market rate of return are 0.056 and 0.125, respectively. According to the capital asset pricing model (CAPM), the expected rate of return on a security with a beta of 1.25 is equal to

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts