Question: 3. Bootstrapping the Zero Curve (16 points total) You observe the following bond prices for bonds with face value $100 and coupons that are paid

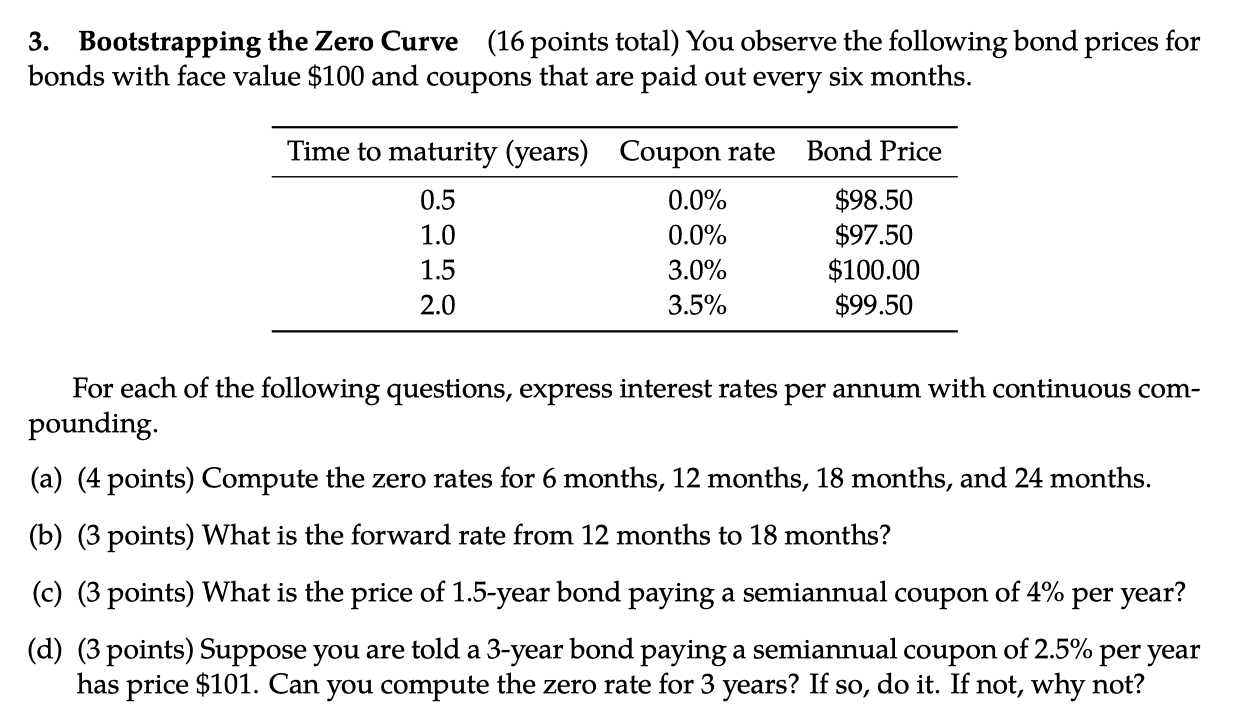

3. Bootstrapping the Zero Curve (16 points total) You observe the following bond prices for bonds with face value $100 and coupons that are paid out every six months. Bond Price Time to maturity (years) Coupon rate 0.5 0.0% 1.0 0.0% 1.5 3.0% 2.0 3.5% $98.50 $97.50 $100.00 $99.50 For each of the following questions, express interest rates per annum with continuous com- pounding (a) (4 points) Compute the zero rates for 6 months, 12 months, 18 months, and 24 months. (b) (3 points) What is the forward rate from 12 months to 18 months? (c) (3 points) What is the price of 1.5-year bond paying a semiannual coupon of 4% per year? (d) (3 points) Suppose you are told a 3-year bond paying a semiannual coupon of 2.5% per year has price $101. Can you compute the zero rate for 3 years? If so, do it. If not, why not? (e) (3 points) Suppose you are told a 3-year bond paying an annual coupon of 2.5% per year has price $101. Can you compute the zero rate for 3 years? If so, do it. If not, why not

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts