Question: 3. Complete the table below: Calculate the market value capital structure weights (You can use the book values as a substitute for the market value

3. Complete the table below: Calculate the market value capital structure weights (You can use the book values as a substitute for the market value of debt). Calculate the cost of equity and cost of debt. (Calculate the YTM: given the bond price of 106 for the ten year annual bond, with a coupon rate of 4.375%, given in Exhibit 6). Calculate the Weighted Average Cost of Capital.

3. Complete the table below: Calculate the market value capital structure weights (You can use the book values as a substitute for the market value of debt). Calculate the cost of equity and cost of debt. (Calculate the YTM: given the bond price of 106 for the ten year annual bond, with a coupon rate of 4.375%, given in Exhibit 6). Calculate the Weighted Average Cost of Capital.

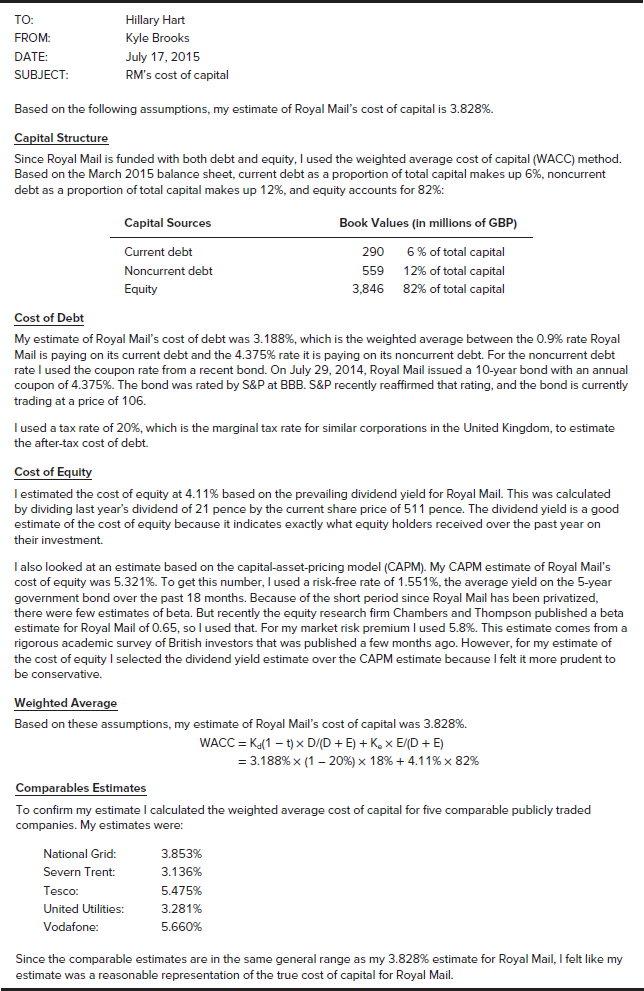

Hillary Hart TO: FROM Kyle Brooks DATE SUBJECT July 17, 2015 RM's cost of capital Based on the following assumptions, my estimate of Royal Mail's cost of capital is 3.828%. Capital Structure Since Royal Mail is funded with both debt and equity, I used the weighted average cost of capital (WACC) method Based on the March 2015 balance sheet, current debt as a proportion of total capital makes up 6%, noncurrent debt as a proportion of total capital makes up 12%, and equity accounts for 82% Capital Sources Book Values (in millions of GBP) 6% of total capital 12% of total capital 82% of total capital Current debt 290 Noncurrent debt 559 Equity 3,846 Cost of Debt My estimate of Royal Mail's cost of debt was 3.188%, which is the weighted average between the 0.9% rate Royal Mail is paying on its current debt and the 4.375% rate it is paying on its noncurrent debt. For the noncurrent debt rate l used the coupon rate from a recent bond. On July 29, 2014, Royal Mail issued a 10-year bond with an annual coupon of 4.375%. The bond was rated by S&P at BBB. S&P recently reaffirmed that rating, and the bond is currently trading at a price of 106 I used a tax rate of 20%, which is the marginal tax rate for similar corporations in the United Kingdom, to estimate the after-tax cost of debt Cost of Equity lestimated the cost of equity at 4.11 % based on the prevailing dividend yield for Royal Mail. This was calculated by dividing last year's dividend of 21 pence by the current share price of 511 pence. The dividend yield is a good estimate of the cost of equity because it indicates exactly what equity holders received over the past year on their investment. I also looked at an estimate based on the capital-asset-pricing model (CAPM). My CAPM estimate of Royal Mail's cost of equity was 5.321%. To get this number, I used a risk-free rate of 1.551%, the average yield on the 5-year government bond over the past 18 months. Because of the short period since Royal Mail has been privatized, there were few estimates of beta. But recently the equity research firm Chambers and Thompson published a beta estimate for Royal Mail of 0.65, so I used that. For my market risk premium I used 5.8%. This estimate comes from a rigorous academic survey of British investors that was published a few months ago. However, for my estimate of the cost of equity selected the dividend yield estimate over the CAPM estimate because I felt it more prudent to be conservative. Weighted Average Based on these assumptions, my estimate of Royal Mail's cost of capital was 3.828% WACC Ka(1t) x D/(D E) K x E/(D E =3.188% x (1-20 % ) x 18 % + 4.1 1% x 82% Comparables Estimates To confirm my estimate I calculated the weighted average cost of capital for five comparable publicly traded companies. My estimates were: National Grid: 3.853% Severn Trent 3.136% 5.475% Tesco: United Utilities: 3.281% Vodafone: 5.660% Since the comparable estimates are in the same general range as my 3.828% estimate for Royal Mail, I felt like my estimate was a reasonable representation of the true cost of capital for Royal Mail. Hillary Hart TO: FROM Kyle Brooks DATE SUBJECT July 17, 2015 RM's cost of capital Based on the following assumptions, my estimate of Royal Mail's cost of capital is 3.828%. Capital Structure Since Royal Mail is funded with both debt and equity, I used the weighted average cost of capital (WACC) method Based on the March 2015 balance sheet, current debt as a proportion of total capital makes up 6%, noncurrent debt as a proportion of total capital makes up 12%, and equity accounts for 82% Capital Sources Book Values (in millions of GBP) 6% of total capital 12% of total capital 82% of total capital Current debt 290 Noncurrent debt 559 Equity 3,846 Cost of Debt My estimate of Royal Mail's cost of debt was 3.188%, which is the weighted average between the 0.9% rate Royal Mail is paying on its current debt and the 4.375% rate it is paying on its noncurrent debt. For the noncurrent debt rate l used the coupon rate from a recent bond. On July 29, 2014, Royal Mail issued a 10-year bond with an annual coupon of 4.375%. The bond was rated by S&P at BBB. S&P recently reaffirmed that rating, and the bond is currently trading at a price of 106 I used a tax rate of 20%, which is the marginal tax rate for similar corporations in the United Kingdom, to estimate the after-tax cost of debt Cost of Equity lestimated the cost of equity at 4.11 % based on the prevailing dividend yield for Royal Mail. This was calculated by dividing last year's dividend of 21 pence by the current share price of 511 pence. The dividend yield is a good estimate of the cost of equity because it indicates exactly what equity holders received over the past year on their investment. I also looked at an estimate based on the capital-asset-pricing model (CAPM). My CAPM estimate of Royal Mail's cost of equity was 5.321%. To get this number, I used a risk-free rate of 1.551%, the average yield on the 5-year government bond over the past 18 months. Because of the short period since Royal Mail has been privatized, there were few estimates of beta. But recently the equity research firm Chambers and Thompson published a beta estimate for Royal Mail of 0.65, so I used that. For my market risk premium I used 5.8%. This estimate comes from a rigorous academic survey of British investors that was published a few months ago. However, for my estimate of the cost of equity selected the dividend yield estimate over the CAPM estimate because I felt it more prudent to be conservative. Weighted Average Based on these assumptions, my estimate of Royal Mail's cost of capital was 3.828% WACC Ka(1t) x D/(D E) K x E/(D E =3.188% x (1-20 % ) x 18 % + 4.1 1% x 82% Comparables Estimates To confirm my estimate I calculated the weighted average cost of capital for five comparable publicly traded companies. My estimates were: National Grid: 3.853% Severn Trent 3.136% 5.475% Tesco: United Utilities: 3.281% Vodafone: 5.660% Since the comparable estimates are in the same general range as my 3.828% estimate for Royal Mail, I felt like my estimate was a reasonable representation of the true cost of capital for Royal Mail

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts