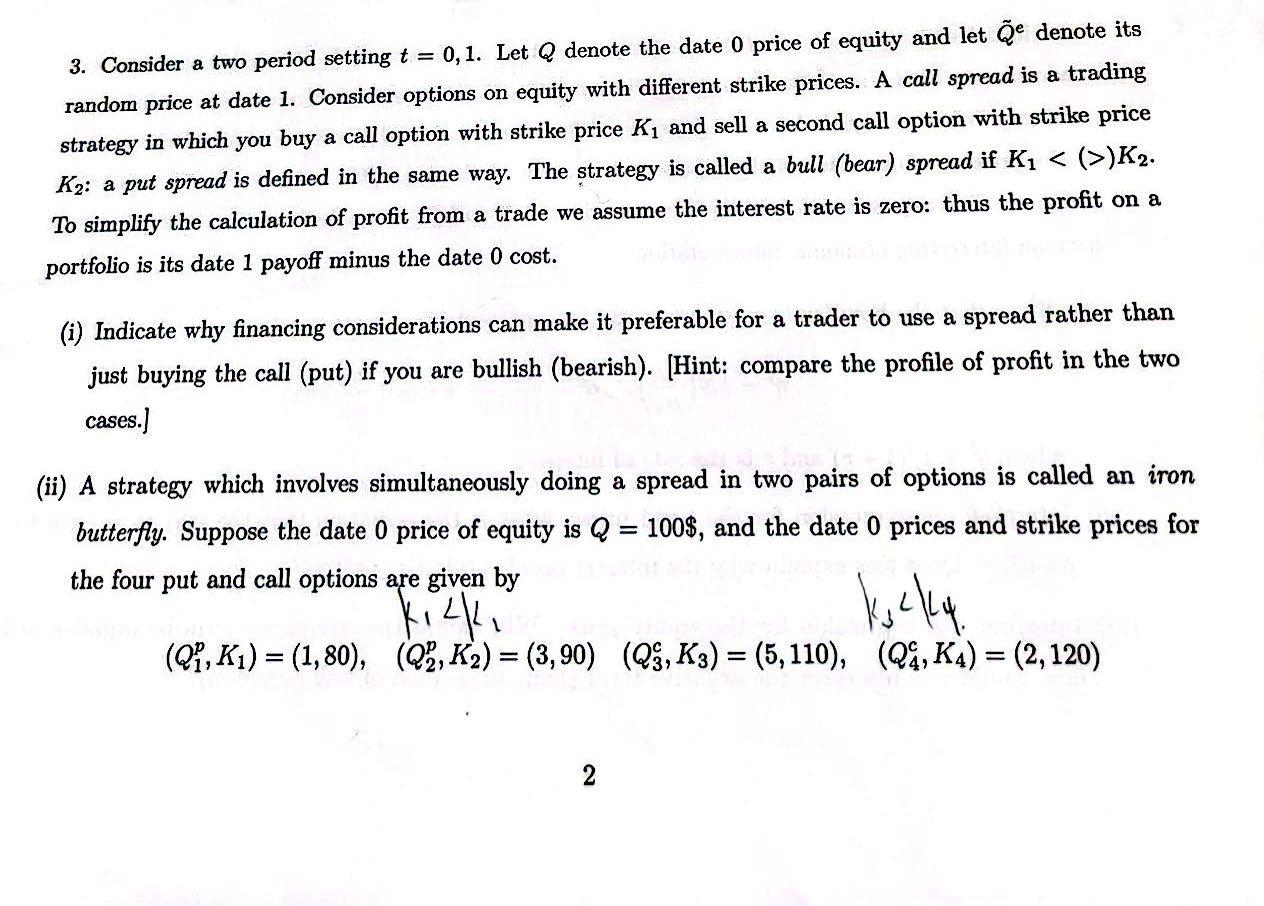

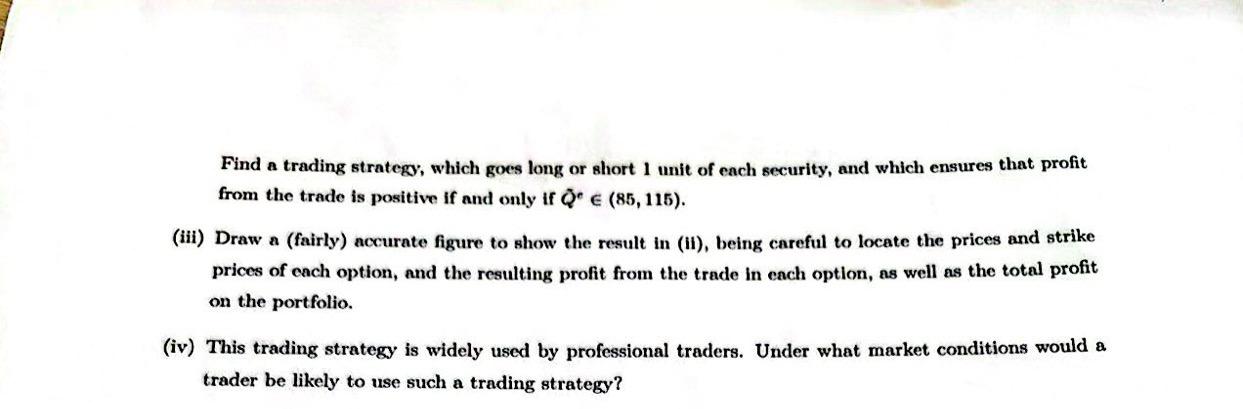

Question: 3. Consider a two period setting t=0, 1. Let Q denote the date 0 price of equity and let Q~e denote its random price at

3. Consider a two period setting t=0, 1. Let Q denote the date 0 price of equity and let Q~e denote its random price at date 1 . Consider options on equity with different strike prices. A call spread is a trading strategy in which you buy a call option with strike price K1 and sell a second call option with strike price K2 : a put spread is defined in the same way. The strategy is called a bull (bear) spread if K1)K2. To simplify the calculation of profit from a trade we assume the interest rate is zero: thus the profit on a portfolio is its date 1 payoff minus the date 0 cost. (i) Indicate why financing considerations can make it preferable for a trader to use a spread rather than just buying the call (put) if you are bullish (bearish). [Hint: compare the profile of profit in the two cases.] (ii) A strategy which involves simultaneously doing a spread in two pairs of options is called an iron butterfly. Suppose the date 0 price of equity is Q=100$, and the date 0 prices and strike prices for the four put and call options are given by (Q1p,K1)=(1,80),(Q2p,K2)=(3,90)(Q3c,K3)=(5,110),(Q4c,K4)=(2,120) 2 Find a trading strategy, which goes long or short 1 unit of each security, and which ensures that profit from the trade is positive if and only if Q^e(85,115). (iii) Draw a (fairly) accurate figure to show the result in (ii), being careful to locate the prices and strike prices of each option, and the resulting profit from the trade in each option, as well as the total profit on the portfolio. iv) This trading strategy is widely used by professional traders. Under what market conditions would a trader be likely to use such a trading strategy? 3. Consider a two period setting t=0, 1. Let Q denote the date 0 price of equity and let Q~e denote its random price at date 1 . Consider options on equity with different strike prices. A call spread is a trading strategy in which you buy a call option with strike price K1 and sell a second call option with strike price K2 : a put spread is defined in the same way. The strategy is called a bull (bear) spread if K1)K2. To simplify the calculation of profit from a trade we assume the interest rate is zero: thus the profit on a portfolio is its date 1 payoff minus the date 0 cost. (i) Indicate why financing considerations can make it preferable for a trader to use a spread rather than just buying the call (put) if you are bullish (bearish). [Hint: compare the profile of profit in the two cases.] (ii) A strategy which involves simultaneously doing a spread in two pairs of options is called an iron butterfly. Suppose the date 0 price of equity is Q=100$, and the date 0 prices and strike prices for the four put and call options are given by (Q1p,K1)=(1,80),(Q2p,K2)=(3,90)(Q3c,K3)=(5,110),(Q4c,K4)=(2,120) 2 Find a trading strategy, which goes long or short 1 unit of each security, and which ensures that profit from the trade is positive if and only if Q^e(85,115). (iii) Draw a (fairly) accurate figure to show the result in (ii), being careful to locate the prices and strike prices of each option, and the resulting profit from the trade in each option, as well as the total profit on the portfolio. iv) This trading strategy is widely used by professional traders. Under what market conditions would a trader be likely to use such a trading strategy

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts