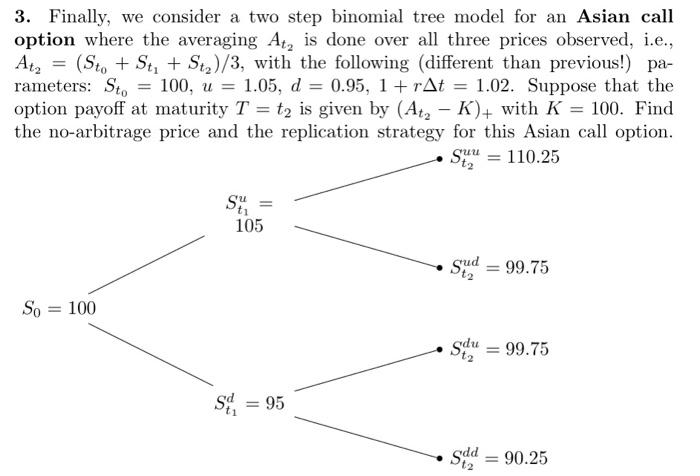

Question: 3. Finally, we consider a two step binomial tree model for an Asian call option where the averaging At2 is done over all three prices

3. Finally, we consider a two step binomial tree model for an Asian call option where the averaging At2 is done over all three prices observed, i.e., At2=(St0+St1+St2)/3, with the following (different than previous!) parameters: St0=100,u=1.05,d=0.95,1+rt=1.02. Suppose that the option payoff at maturity T=t2 is given by (At2K)+with K=100. Find the no-arbitrage price and the replication strategy for this Asian call option. 3. Finally, we consider a two step binomial tree model for an Asian call option where the averaging At2 is done over all three prices observed, i.e., At2=(St0+St1+St2)/3, with the following (different than previous!) parameters: St0=100,u=1.05,d=0.95,1+rt=1.02. Suppose that the option payoff at maturity T=t2 is given by (At2K)+with K=100. Find the no-arbitrage price and the replication strategy for this Asian call option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts