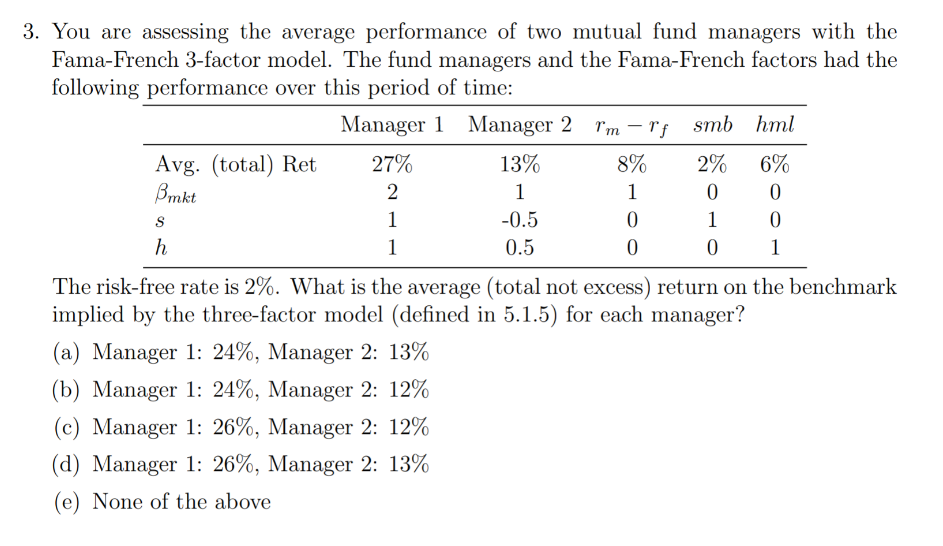

Question: 3. You are assessing the average performance of two mutual fund managers with the Fama-French 3-factor model. The fund managers and the Fama-French factors had

3. You are assessing the average performance of two mutual fund managers with the Fama-French 3-factor model. The fund managers and the Fama-French factors had the following performance over this period of time: The risk-free rate is 2%. What is the average (total not excess) return on the benchmark implied by the three-factor model (defined in 5.1.5) for each manager? (a) Manager 1: 24\%, Manager 2: 13% (b) Manager 1: 24\%, Manager 2: 12% (c) Manager 1: 26\%, Manager 2: 12% (d) Manager 1: 26\%, Manager 2: 13% (e) None of the above

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock