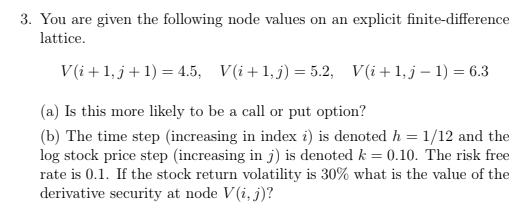

Question: 3. You given the following node values on an explicit finite-difference are lattice V(i1,j14.5, V(i+1,j)= 5.2, V(i+1,j - 1) 6.3 (a) Is this more likely

3. You given the following node values on an explicit finite-difference are lattice V(i1,j14.5, V(i+1,j)= 5.2, V(i+1,j - 1) 6.3 (a) Is this more likely to be a call or put option? (b) The time step (increasing in index i) is denoted h = 1/12 and the log stock price step (increasing in j) is denoted k = 0.10. The risk free rate is 0.1. If the stock return volatility is 30% what is the value of the derivative security at node V(i, j)? 3. You given the following node values on an explicit finite-difference are lattice V(i1,j14.5, V(i+1,j)= 5.2, V(i+1,j - 1) 6.3 (a) Is this more likely to be a call or put option? (b) The time step (increasing in index i) is denoted h = 1/12 and the log stock price step (increasing in j) is denoted k = 0.10. The risk free rate is 0.1. If the stock return volatility is 30% what is the value of the derivative security at node V(i, j)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts