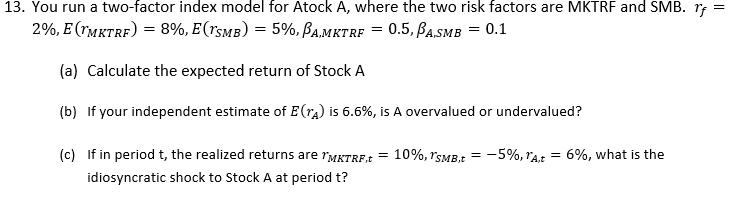

Question: 3. You run a two-factor index model for Atock A, where the two risk factors are MKTRF and SMB. rf= 2%,E(rMKTRF)=8%,E(rSMB)=5%,A,MKTRF=0.5,A,SMB=0.1 (a) Calculate the expected

3. You run a two-factor index model for Atock A, where the two risk factors are MKTRF and SMB. rf= 2%,E(rMKTRF)=8%,E(rSMB)=5%,A,MKTRF=0.5,A,SMB=0.1 (a) Calculate the expected return of Stock A (b) If your independent estimate of E(rA) is 6.6%, is A overvalued or undervalued? (c) If in period t, the realized returns are rMKTRF,t=10%,rSMB,t=5%,rA,t=6%, what is the idiosyncratic shock to Stock A at period t

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock