Question: 31.a b. c. d. e. Suppose that you bought a 10-year annual coupon bond with 8% coupon rate and a face value of $1000. At

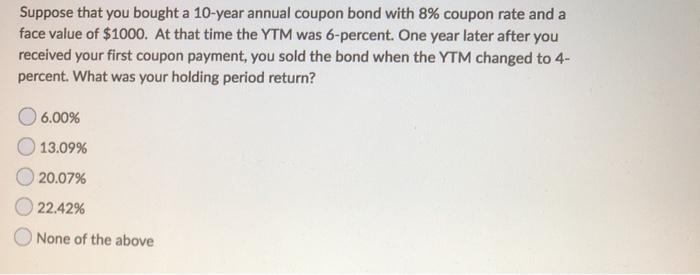

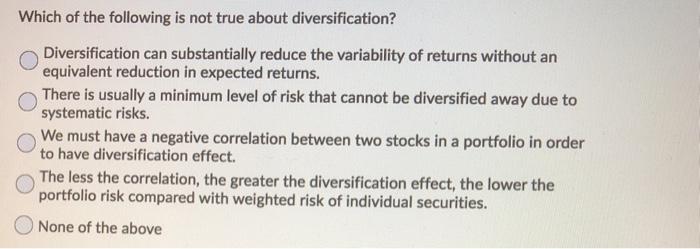

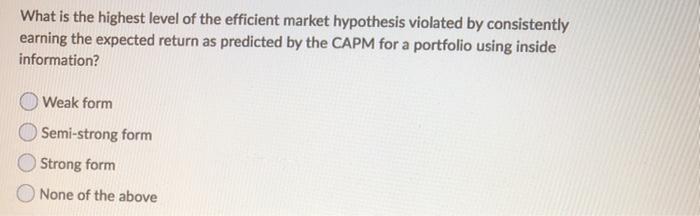

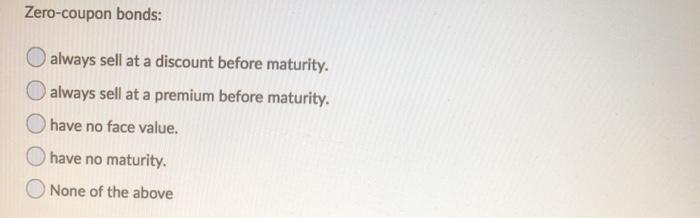

Suppose that you bought a 10-year annual coupon bond with 8% coupon rate and a face value of $1000. At that time the YTM was 6-percent. One year later after you received your first coupon payment, you sold the bond when the YTM changed to 4- percent. What was your holding period return? 6.00% 13.09% 20.07% 22.42% None of the above Which of the following is not true about diversification? Diversification can substantially reduce the variability of returns without an equivalent reduction in expected returns. There is usually a minimum level of risk that cannot be diversified away due to systematic risks. We must have a negative correlation between two stocks in a portfolio in order to have diversification effect. The less the correlation, the greater the diversification effect, the lower the portfolio risk compared with weighted risk of individual securities. None of the above What is the highest level of the efficient market hypothesis violated by consistently earning the expected return as predicted by the CAPM for a portfolio using inside information? Weak form Semi-strong form Strong form None of the above Zero-coupon bonds: always sell at a discount before maturity. always sell at a premium before maturity. have no face value. have no maturity. O None of the above Given a lump sum in the future, the more frequent the compounding the Ogreater the present value. O greater the effective annual interest rate. greater the future value. lesser the future value. None of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts