Question: 33830: stebdo3: 3 = A CHARTERED ; : Bo COMPTABLES = oe PROFESSIONAL ee A PROFESSIONNELS LF fos I ACCOUNTANTS | Cc Nene ee ere

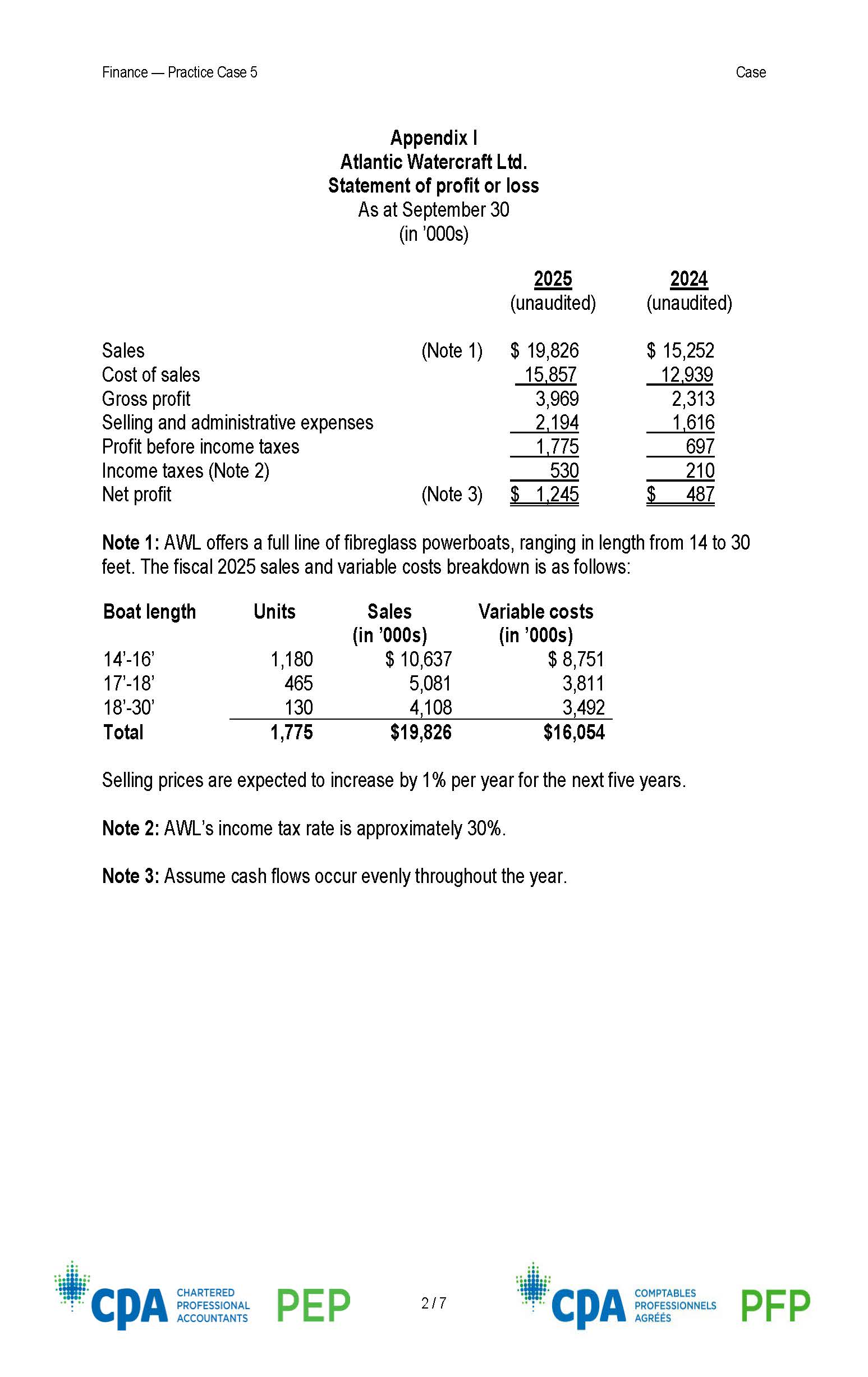

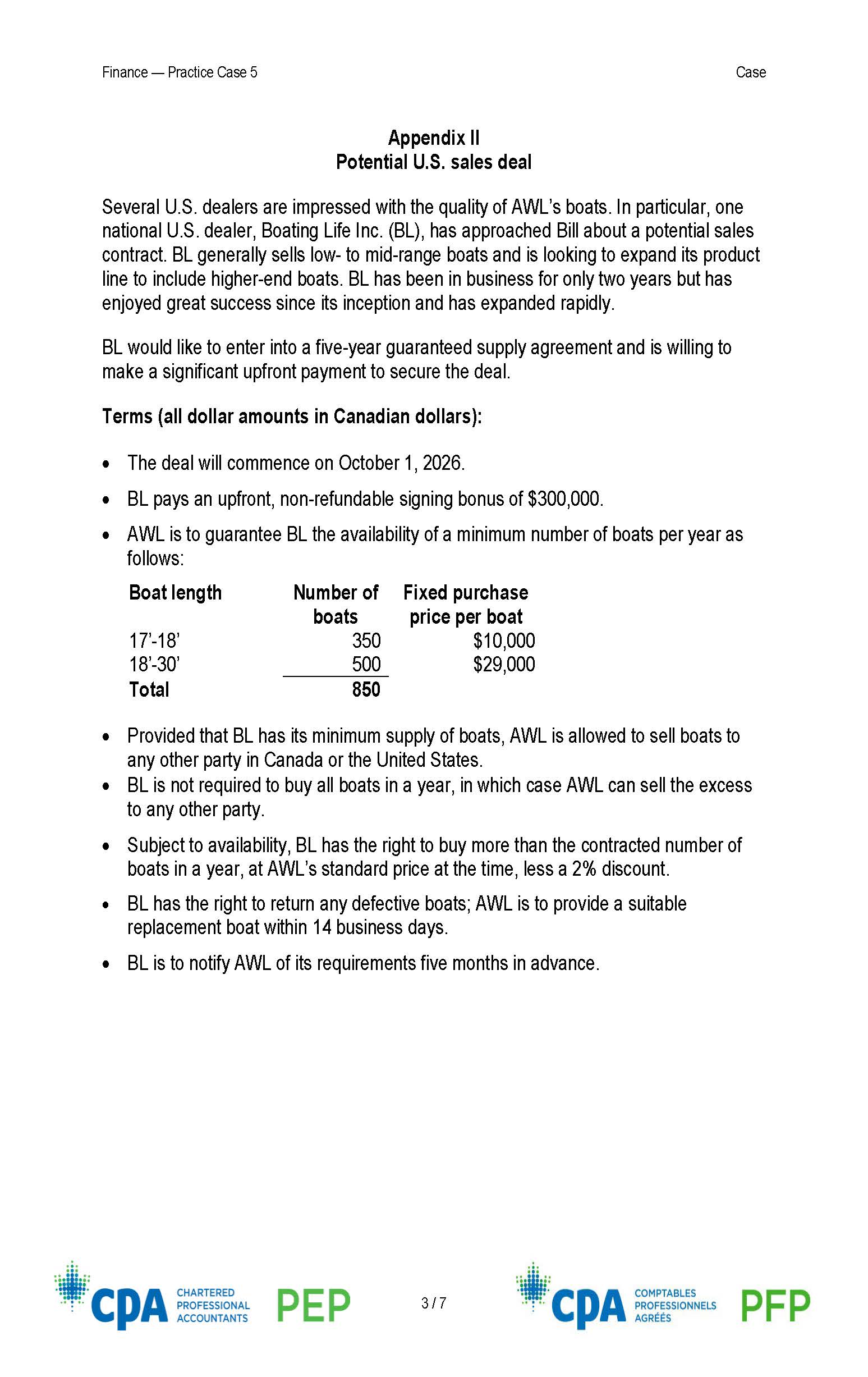

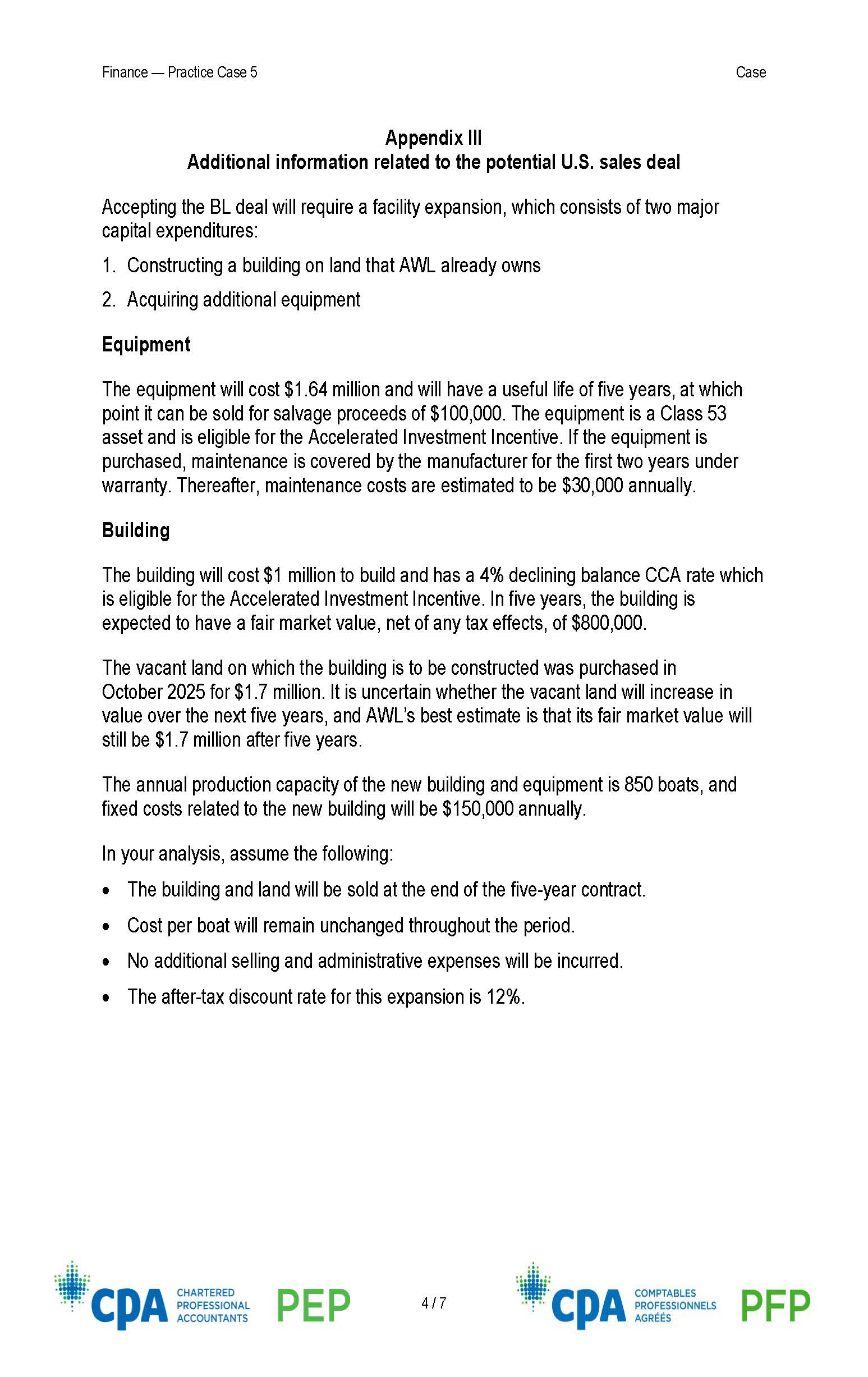

33830: stebdo3: 3 = A CHARTERED ; : Bo COMPTABLES = oe PROFESSIONAL ee A PROFESSIONNELS LF fos I ACCOUNTANTS | Cc Nene ee ere Finance Practice Case 5 Case (120 minutes) Atlantic Watercraft Limited (AWL) is a privately owned Canadian powerboat manufacturer. AVVL was incorporated 25 years ago by three brothers, John, Mark, and Harry Smith, who each own one-third of the common shares. Bill Smith, John's son, has recently been appointed president and chief operating officer of the company. To date, AWL has followed a very successful operating strategy of producing high-quality boats. Revenues and net income have grown significantly in the past year, as shown in AWL's statement of profit or loss (Appendix I). Currently the company is at capacity and has a long waitlist of customers looking to purchase boats. Bill is young and aggressive, and believes that AWL should expand its operations to capture potential sales in the U.S. market. In fact, he has secured a potential sales deal with a large U.S. dealer (Appendix Il). If AWWL proceeds with the U.S. sales deal, it will need to increase its capacity, requiring an investment in a new building and new equipment. Additional information related to the potential U.S. sales deal is included in Appendix Ill. It is now November 2025 and the brothers have approached your firm, Richards & Gibbs, Chartered Professional Accountants, for advice. You, CPA, are in charge of the AWV/L engagement. Specifically, the brothers are looking for an analysis of whether to accept the U.S. sales deal. AWL can either use bank financing to purchase the equipment or lease it through the vendor (Appendix IV'). Before analyzing the U.S. sales deal, the brothers are wondering whether they should lease or buy the equipment. You should incorporate your recommendation to lease or buy into your analysis of the US. sales deal. Lastly, at the end of your meeting with the brothers, Harry wondered if AWL should increase its prices for its Canadian customers given the success of the company over the last year. This is a separate decision from the decision to pursue the U.S. sales deal. He proposed a 10% price increase for Canadian customers (Appendix V), and you agreed to provide an analysis of such a price change. Your response should be no longer than 3,600 words, excluding any Excel files. Chartered Professional Accountants of Canada. All rights reserved. No part of this publication may be reproduced or transmitted, in any form or by any means, without the prior written consent of CPA Canada. For information regarding permissions, please contact permissions@cpacanada.ca. 2024-12-11 Finance Practice Case 5 Case Appendix | Atlantic Watercraft Ltd. Statement of profit or loss As at September 30 (in 'O00s) 2025 2024 (unaudited) (unaudited) Sales (Note 1) $ 19,826 $ 15,252 Cost of sales 15,857 12,939 Gross profit 3,969 2,313 Selling and administrative expenses 2,194 1,616 Profit before income taxes 1,775 697 Income taxes (Note 2) 530 210 Net profit (Note 3) $ 1,245 $ 487 Note 1: AVVL offers a full line of fibreglass powerboats, ranging in length from 14 to 30 feet. The fiscal 2025 sales and variable costs breakdown is as follows: Boat length Units Sales Variable costs (in 000s) (in '000s) 14'-16' 1,180 $ 10,637 $ 8,751 17-18' 465 5,081 3,811 18'-30' 130 4,108 3,492 Total 1,775 $19,826 $16,054 Selling prices are expected to increase by 1% per year for the next five years. Note 2: AWL's income tax rate is approximately 30%. Note 3: Assume cash flows occur evenly throughout the year. sede seaddae:: Ha: CHARTERED \"TERRE. COMPTABLES eS rm PROFESSIONAL 2/7 meee PROFESSIONNELS aD fim fad ACCOUNTANTS AGREES a l Finance - Practice Case 5 Case Appendix II Potential U.S. sales deal Several U.S. dealers are impressed with the quality of AWL's boats. In particular, one national U.S. dealer, Boating Life Inc. (BL), has approached Bill about a potential sales contract. BL generally sells low- to mid-range boats and is looking to expand its product line to include higher-end boats. BL has been in business for only two years but has enjoyed great success since its inception and has expanded rapidly. BL would like to enter into a five-year guaranteed supply agreement and is willing to make a significant upfront payment to secure the deal. Terms (all dollar amounts in Canadian dollars): . The deal will commence on October 1, 2026. . BL pays an upfront, non-refundable signing bonus of $300,000. . AWL is to guarantee BL the availability of a minimum number of boats per year as follows: Boat length Number of Fixed purchase boats price per boat 17'-18' 350 $10,000 18'-30' 500 $29,000 Total 850 Provided that BL has its minimum supply of boats, AWL is allowed to sell boats to any other party in Canada or the United States. . BL is not required to buy all boats in a year, in which case AWL can sell the excess to any other party. . Subject to availability, BL has the right to buy more than the contracted number of boats in a year, at AWL's standard price at the time, less a 2% discount. . BL has the right to return any defective boats; AWL is to provide a suitable replacement boat within 14 business days . BL is to notify AWL of its requirements five months in advance. CPA CHARTERED PEP 3/7 CPA COMPTABLES ROFESSIONAL PROFESSIONNELS ACCOUNTANTS AGREES PFPFinance Practice Case 5 Case Appendix Ill Additional information related to the potential U.S. sales deal Accepting the BL deal will require a facility expansion, which consists of two major capital expenditures: 1. Constructing a building on land that AWL already owns 2. Acquiring additional equipment Equipment The equipment will cost $1.64 million and will have a useful life of five years, at which point it can be sold for salvage proceeds of $100,000. The equipment is a Class 53 asset and is eligible for the Accelerated Investment Incentive. If the equipment is purchased, maintenance is covered by the manufacturer for the first two years under warranty. Thereafter, maintenance costs are estimated to be $30,000 annually. Building The building will cost $1 million to build and has a 4% declining balance CCA rate which is eligible for the Accelerated Investment Incentive. In five years, the building is expected to have a fair market value, net of any tax effects, of $800,000. The vacant land on which the building is to be constructed was purchased in October 2025 for $1.7 million. It is uncertain whether the vacant land will increase in value over the next five years, and AWL's best estimate is that its fair market value will still be $1.7 million after five years. The annual production capacity of the new building and equipment is 850 boats, and fixed costs related to the new building will be $150,000 annually. In your analysis, assume the following: e The building and land will be sold at the end of the five-year contract. e Cost per boat will remain unchanged throughout the period. e No additional selling and administrative expenses will be incurred. e The after-tax discount rate for this expansion is 12%. : 3: oot. ra Ed Hag: CHARTERED \"EERE COMPTABLES rs = rF PROFESSIONAL 4/7 mies PROFESSIONNELS Lad fas ACCOUNTANTS AGREES u u Finance Practice Case 5 Case Appendix Ill (continued) Additional information related to the potential U.S. sales deal Other considerations The brothers have mixed feelings about Bill's strategy, as they are all very close to retirement. Mark is averse to the use of debt and believes that AVWL's debt-free balance sheet is the reason AWL has survived past recessions while competitors have struggled. John is hesitant but sees the value in the expansion, given the anticipated surge in first-time purchases by affluent baby boomers. Harry is concerned because he is planning to retire within 12 months and wants to ensure the company has sufficient cash to redeem his shares. He is also concerned about the impact on staff. Despite AWL's historically good labour relations, its union has raised concerns about the implications of the increased workload that staff may bear through this increase in production. : 3h. vheseeess i i. CHARTERED \"EERE COMPTABLES ES = re PROFESSIONAL 5/7 meee PROFESSIONNELS aD fim fad ACCOUNTANTS AGREES a l Finance Practice Case 5 Case Appendix IV Financing terms Bank financing The bank is willing to finance the expansion with a five-year loan up to $2,640,000. The terms are as follows: e Interest rate: 10%, payable annually. e Repayment terms: interest only, due December 31 each year. Principal amount due at the end of the five-year term. Although the powerboat industry has experienced a high rate of bankruptcy over the years, because of AWL's strong financial history and positive working relationship with the bank, it will not require any covenants. Lease equipment AWL also has the option to lease the equipment (and just use bank financing for the building). The terms are as follows for the lease: e Term: five years, starting October 1, 2026. e Annual payment: $400,000, payable at the beginning of each year. e End of term: equipment returned to lessor for zero proceeds. e Maintenance: covered by manufacturer for the entire term of the lease. e Maximum machine hours per year: &,500 hours. If the machine hours exceed this amount, penalties will apply. The maximum machine hours are expected to be sufficient to meet the demands of the BL contract. : HH sees. ra Ed sige" CHARTERED \"aR: COMPTABLES > re, PROFESSIONAL 6/7 meee PROFESSIONNELS Bi 2, ACCOUNTANTS AGREES a i} Finance Practice Case 5 Case Appendix V Revised pricing and demand levels With a pricing adjustment, an independent market research consultant has determined that demand will change. A 10% price increase is expected to decrease demand to the following levels: Boat length Anticipated unit sales (% of current sales) 14-16 75-90% 17-18 60-74% Over 18' 50-60% AWVL would like you to consider the pricing revision only on existing sales and separately from the expansion, as the U.S. expansion is at a set contract price that cannot be increased. a i ees RHE. CHARTERED = : \"TERRE. COMPTABLES =, = = PROFESSIONAL , = (if meee PROFESSIONNELS DD foes ACCOUNTANTS f AGREES rei

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To approach the decision regarding Atlantic Watercraft Limited AWL expansion into the US market and ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!