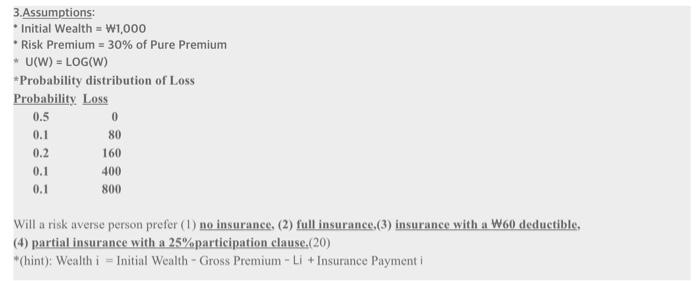

Question: 3.Assumptions: * Initial Wealth = W1,000 Risk Premium = 30% of Pure Premium *U(W) = LOG(W) * Probability distribution of Loss Probability Loss 0 0.1

3.Assumptions: * Initial Wealth = W1,000 Risk Premium = 30% of Pure Premium *U(W) = LOG(W) * Probability distribution of Loss Probability Loss 0 0.1 80 0.5 0.2 160 400 0.1 0.1 800 Will a risk averse person prefer (1) no insurance, (2) full insurance, (3) insurance with a W60 deductible, (4) partial insurance with a 25%participation clause (20) hint): Wealth i = Initial Wealth - Gross Premium - Li + Insurance Payment

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock