Question: 4: 4. Explain the basis risk by deriving the effective price of a long hedge in the following order. However, the starting point of hedging

4:

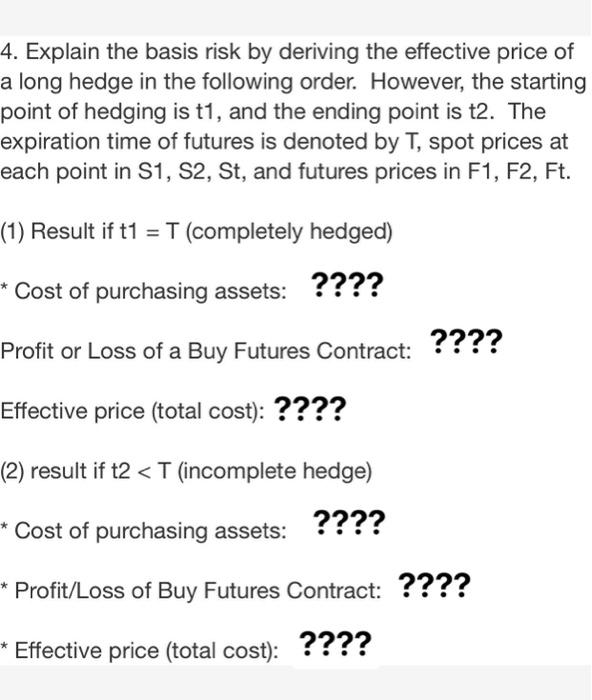

4. Explain the basis risk by deriving the effective price of a long hedge in the following order. However, the starting point of hedging is t1, and the ending point is t2. The expiration time of futures is denoted by T, spot prices at each point in S1, S2, St, and futures prices in F1, F2, Ft. (1) Result if t1 = T (completely hedged) * Cost of purchasing assets: ???? Profit or Loss of a Buy Futures Contract: ???? Effective price (total cost): ???? (2) result if t2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock