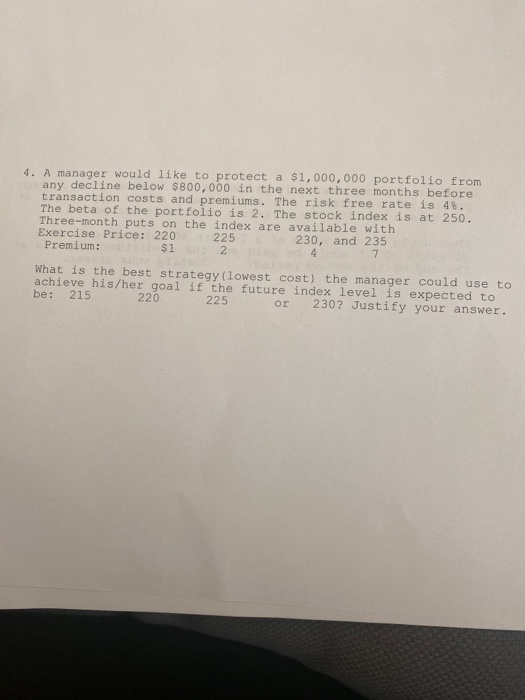

Question: 4. A manager would like to protect a $1,000,000 portfolio from any decline below $800,000 in the next three months before transaction costs and premiums.

4. A manager would like to protect a $1,000,000 portfolio from any decline below $800,000 in the next three months before transaction costs and premiums. The risk free rate is 4%. The beta of the portfolio is 2. The stock index is at 250. Three-month puts on the index are available with Exercise Price: 220 225 230, and 235 Premium: $1 What is the best strategy (lowest cost the manager could use to achieve his/her goal if the future index level is expected to be: 215 220 225 or 230? Justify your

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock