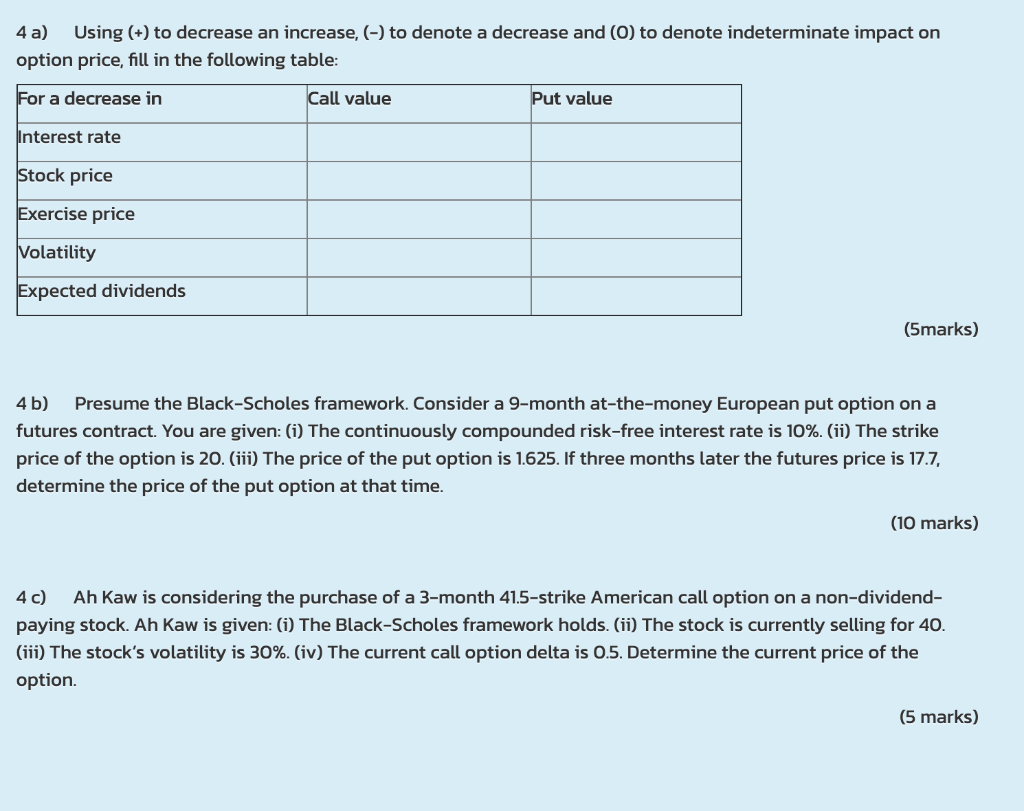

Question: 4 a) Using (+) to decrease an increase, (-) to denote a decrease and (0) to denote indeterminate impact on option price, fill in the

4 a) Using (+) to decrease an increase, (-) to denote a decrease and (0) to denote indeterminate impact on option price, fill in the following table: For a decrease in Call value Put value Interest rate Stock price Exercise price Volatility Expected dividends (5marks) 4b) Presume the Black-Scholes framework. Consider a 9-month at-the-money European put option on a futures contract. You are given: (i) The continuously compounded risk-free interest rate is 10%. (ii) The strike price of the option is 20. (iii) The price of the put option is 1.625. If three months later the futures price is 17.7, determine the price of the put option at that time. (10 marks) 4c) Ah Kaw is considering the purchase of a 3-month 41.5-strike American call option on a non-dividend- paying stock. Ah Kaw is given: (i) The Black-Scholes framework holds. (ii) The stock is currently selling for 40. (iii) The stock's volatility is 30%. (iv) The current call option delta is 0.5. Determine the current price of the option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts