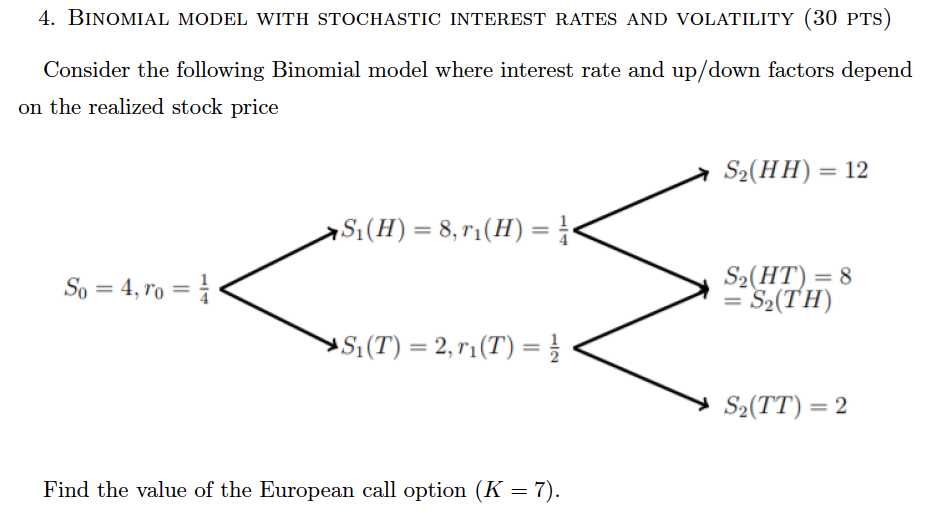

Question: 4. BINOMAL MODEL WITH STOCHASTIC INTEREST RATES AND VOLATILITY (30 PTS) Consider the following Binomial model where interest rate and up/down factors depend on the

4. BINOMAL MODEL WITH STOCHASTIC INTEREST RATES AND VOLATILITY (30 PTS) Consider the following Binomial model where interest rate and up/down factors depend on the realized stock price S2(HH) 12 s,(H) = 8,n(H) = s,(HT) = 8 S(T)-2,r(T)- SATT) = 2 Find the value of the European call option (K7

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock