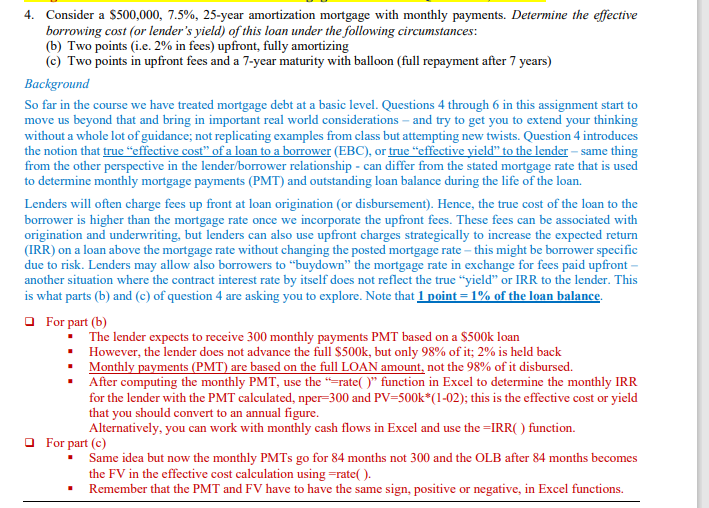

4. Consider a $500,000, 7.5%, 25-year amortization mortgage with monthly payments. Determine the effective borrowing cost...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

b Two points upfront fully amortizing Loan amount 500000 Points fees 2 of 50... View the full answer

Related Book For

Real Estate Principles A Value Approach

ISBN: 978-0077836368

5th edition

Authors: David C Ling, Wayne Archer

Posted Date: