Question: 4. Consider a world in which there are exactly two assets (labelled A and B) and two states of nature (labelled 1 and 2). The

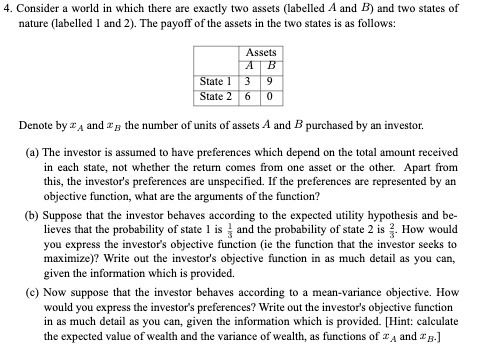

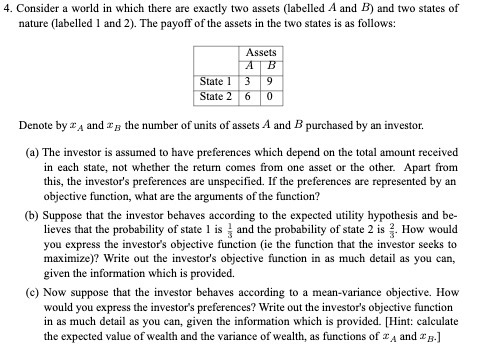

4. Consider a world in which there are exactly two assets (labelled A and B) and two states of nature (labelled 1 and 2). The payoff of the assets in the two states is as follows: Assets B State 1 9 State 2 6 Denote by 2 4 and 25 the number of units of assets A and B purchased by an investor. (a) The investor is assumed to have preferences which depend on the total amount received in each state, not whether the return comes from one asset or the other. Apart from this, the investor's preferences are unspecified. If the preferences are represented by an objective function, what are the arguments of the function? (b) Suppose that the investor behaves according to the expected utility hypothesis and be- lieves that the probability of state I is , and the probability of state 2 is 2. How would you express the investor's objective function (ie the function that the investor seeks to maximize)? Write out the investor's objective function in as much detail as you can, given the information which is provided. (c) Now suppose that the investor behaves according to a mean-variance objective. How would you express the investor's preferences? Write out the investor's objective function in as much detail as you can, given the information which is provided. [ Hint: calculate the expected value of wealth and the variance of wealth, as functions of 24 and ~ g.]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts