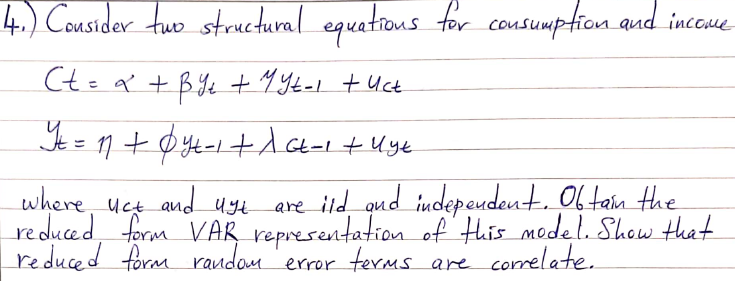

Question: 4.) Cousider two structural equations for consumption and income Ct = a + 8y + Myt-1 + Uct Yt = 1 + 0yt-1 + A

4.) Cousider two structural equations for consumption and income Ct = a + 8y + Myt-1 + Uct Yt = 1 + 0yt-1 + A Gt-1 + uyt where uct and us are ild and independent. Obtain the reduced form VAR representation of this model. Show that reduced form random error terms are correlate. 4.) Cousider two structural equations for consumption and income Ct = a + 8y + Myt-1 + Uct Yt = 1 + 0yt-1 + A Gt-1 + uyt where uct and us are ild and independent. Obtain the reduced form VAR representation of this model. Show that reduced form random error terms are correlate

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock