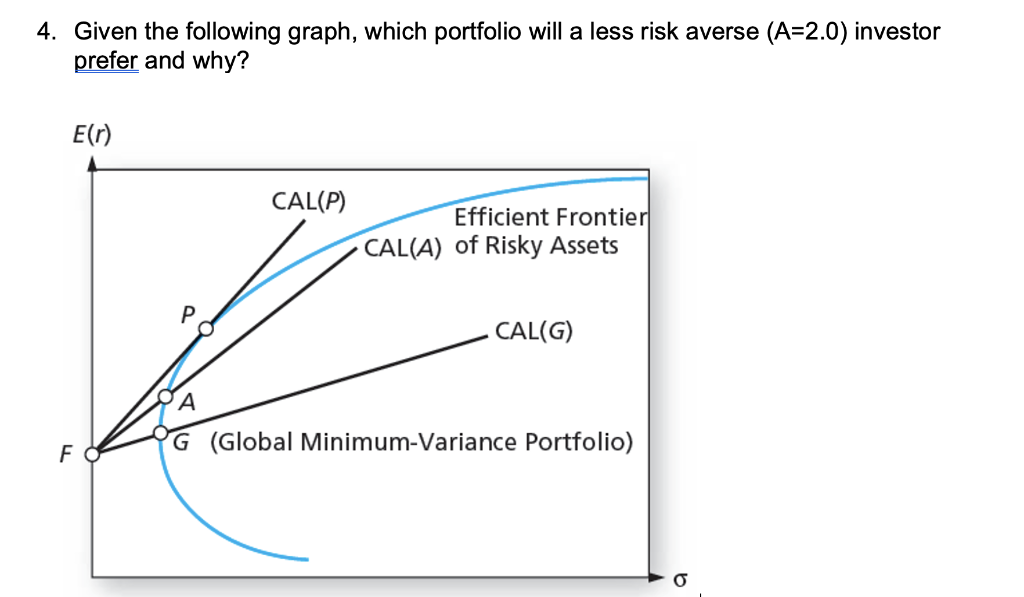

Question: 4. Given the following graph, which portfolio will a less risk averse (A=2.0) investor prefer and why? E() CAL(P) Efficient Frontier CAL(A) of Risky Assets

4. Given the following graph, which portfolio will a less risk averse (A=2.0) investor prefer and why? E() CAL(P) Efficient Frontier CAL(A) of Risky Assets CAL(G) A FO G (Global Minimum-Variance Portfolio)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock