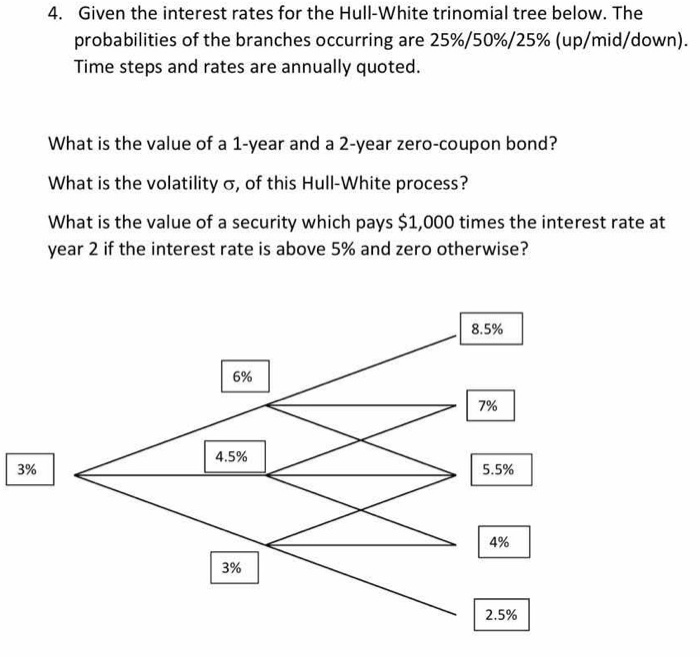

Question: 4. Given the interest rates for the Hull-White trinomial tree below. The probabilities of the branches occurring are 25%/50%/25% (up/mid/down). Time steps and rates are

4. Given the interest rates for the Hull-White trinomial tree below. The probabilities of the branches occurring are 25%/50%/25% (up/mid/down). Time steps and rates are annually quoted. What is the value of a 1-year and a 2-year zero-coupon bond? What is the volatility o, of this Hull-White process? What is the value of a security which pays $1,000 times the interest rate at year 2 if the interest rate is above 5% and zero otherwise? 8.5% 6% 7% 4.5% 3% 5.5% 4% 2.5% 4. Given the interest rates for the Hull-White trinomial tree below. The probabilities of the branches occurring are 25%/50%/25% (up/mid/down). Time steps and rates are annually quoted. What is the value of a 1-year and a 2-year zero-coupon bond? What is the volatility o, of this Hull-White process? What is the value of a security which pays $1,000 times the interest rate at year 2 if the interest rate is above 5% and zero otherwise? 8.5% 6% 7% 4.5% 3% 5.5% 4% 2.5%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts