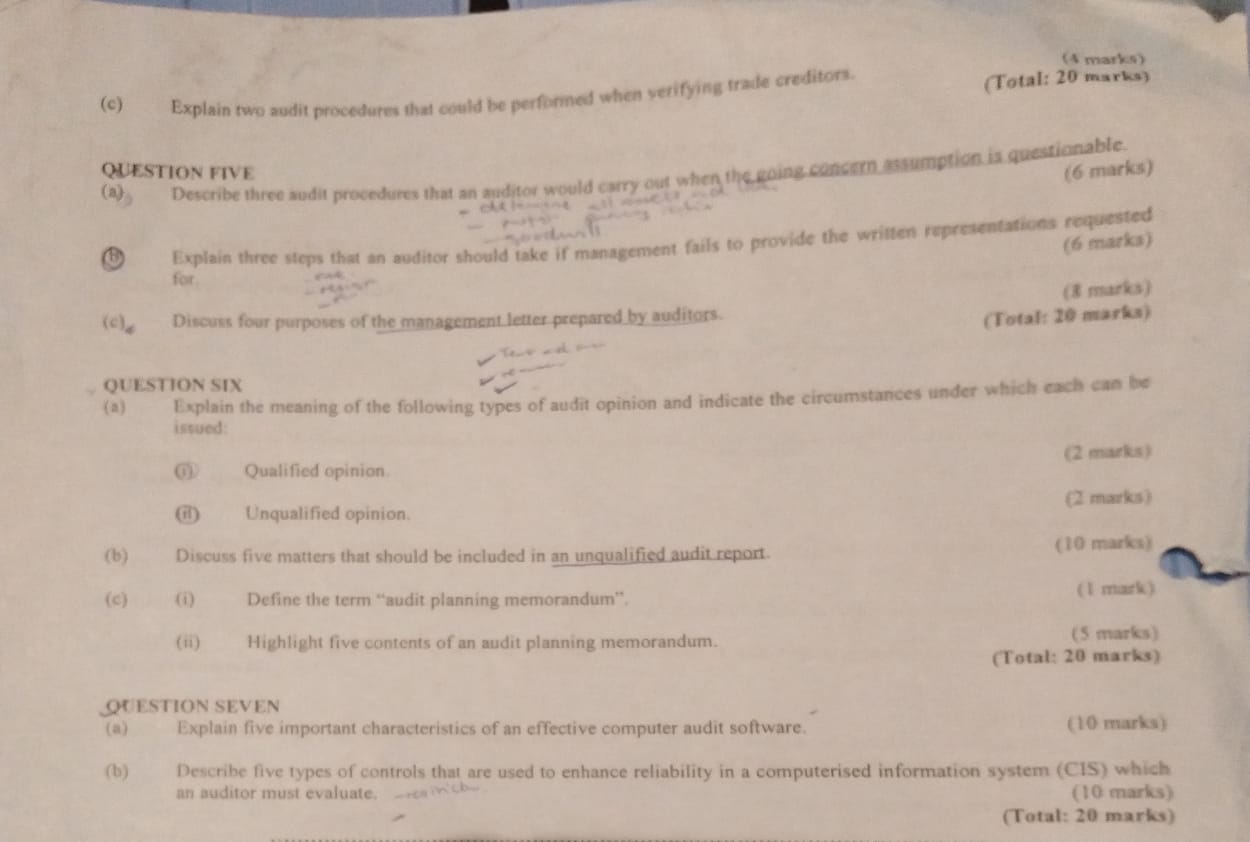

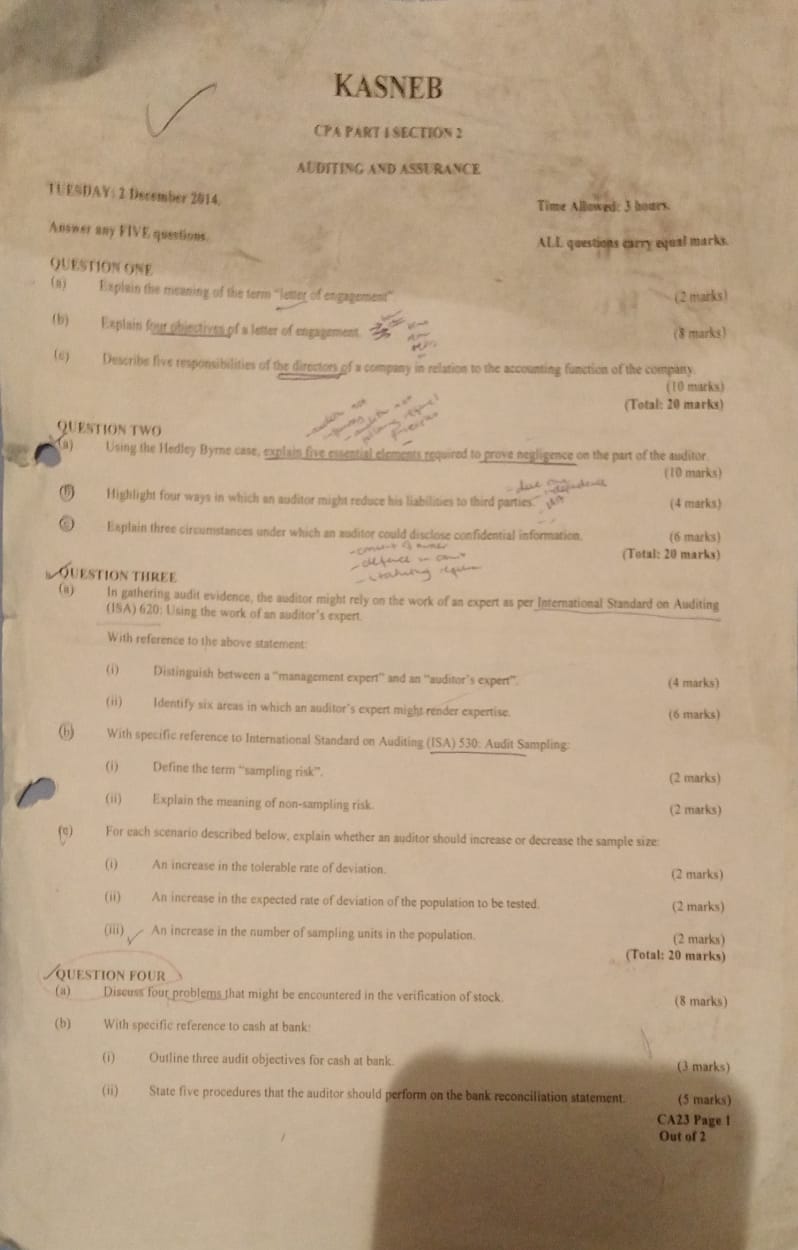

Question: (4 marks) (c) Explain two audit procedures that could be performed when verifying trade creditors. (Total: 20 marks) QUESTION FIVE (a) Describe three audit procedures

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock