Question: 4. Option pricing - Multiperiod binomial approach Aa Aa The value of an option can be calculated by using a step-by-step approach in the case

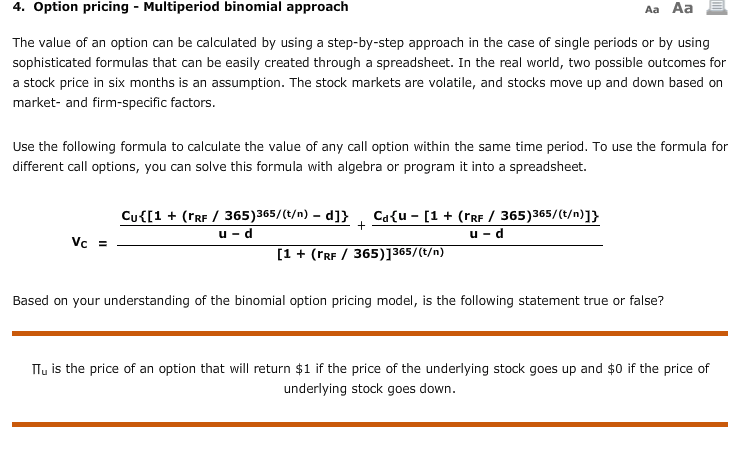

4. Option pricing - Multiperiod binomial approach Aa Aa The value of an option can be calculated by using a step-by-step approach in the case of single periods or by using sophisticated formulas that can be easily created through a spreadsheet. In the real world, two possible outcomes for a stock price in six months is an assumption. The stock markets are volatile, and stocks move up and down based on market- and firm-specific factors. Use the following formula to calculate the value of any call option within the same time period. To use the formula for different call options, you can solve this formula with algebra or program it into a spreadsheet. Cu{[1 + (TRF / 365)365/(t) - d]} Ca{u - [1 + (rRF / 365 365/(t)]} + u-d U-d Vc = [1 + (CRF / 36521365/(t) Based on your understanding of the binomial option pricing model, is the following statement true or false? Hy is the price of an option that will return $1 if the price of the underlying stock goes up and $0 if the price of underlying stock goes down. 4. Option pricing - Multiperiod binomial approach Aa Aa The value of an option can be calculated by using a step-by-step approach in the case of single periods or by using sophisticated formulas that can be easily created through a spreadsheet. In the real world, two possible outcomes for a stock price in six months is an assumption. The stock markets are volatile, and stocks move up and down based on market- and firm-specific factors. Use the following formula to calculate the value of any call option within the same time period. To use the formula for different call options, you can solve this formula with algebra or program it into a spreadsheet. Cu{[1 + (TRF / 365)365/(t) - d]} Ca{u - [1 + (rRF / 365 365/(t)]} + u-d U-d Vc = [1 + (CRF / 36521365/(t) Based on your understanding of the binomial option pricing model, is the following statement true or false? Hy is the price of an option that will return $1 if the price of the underlying stock goes up and $0 if the price of underlying stock goes down

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts