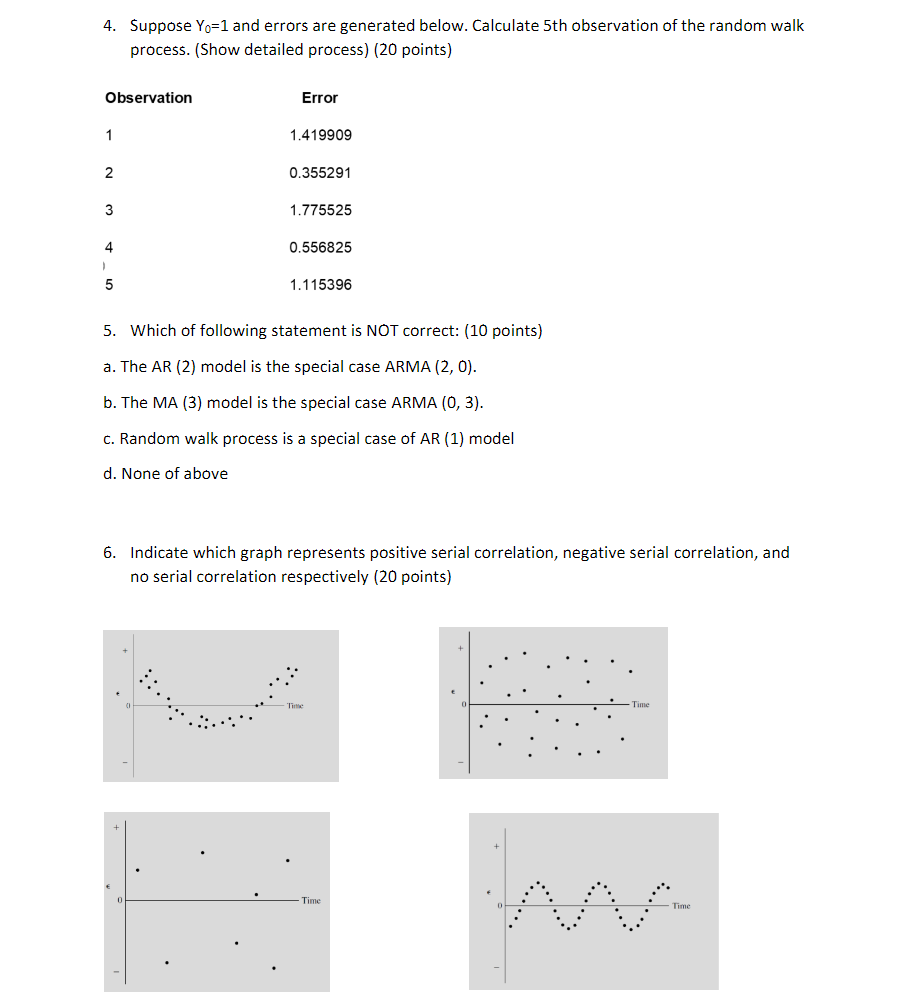

Question: 4. Suppose Yo=1 and errors are generated below. Calculate 5th observation of the random walk process. (Show detailed process) (20 points) Observation 1 Error

4. Suppose Yo=1 and errors are generated below. Calculate 5th observation of the random walk process. (Show detailed process) (20 points) Observation 1 Error 1.419909 2 0.355291 3 1.775525 4 0.556825 ' 5 1.115396 5. Which of following statement is NOT correct: (10 points) a. The AR (2) model is the special case ARMA (2, 0). b. The MA (3) model is the special case ARMA (0, 3). c. Random walk process is a special case of AR (1) model d. None of above 6. Indicate which graph represents positive serial correlation, negative serial correlation, and no serial correlation respectively (20 points) Time Time Time

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts