Question: 4. Using the following data to answer the questions A.Plot the yield curve using spot zero rates, where the interest rates are based on continuous

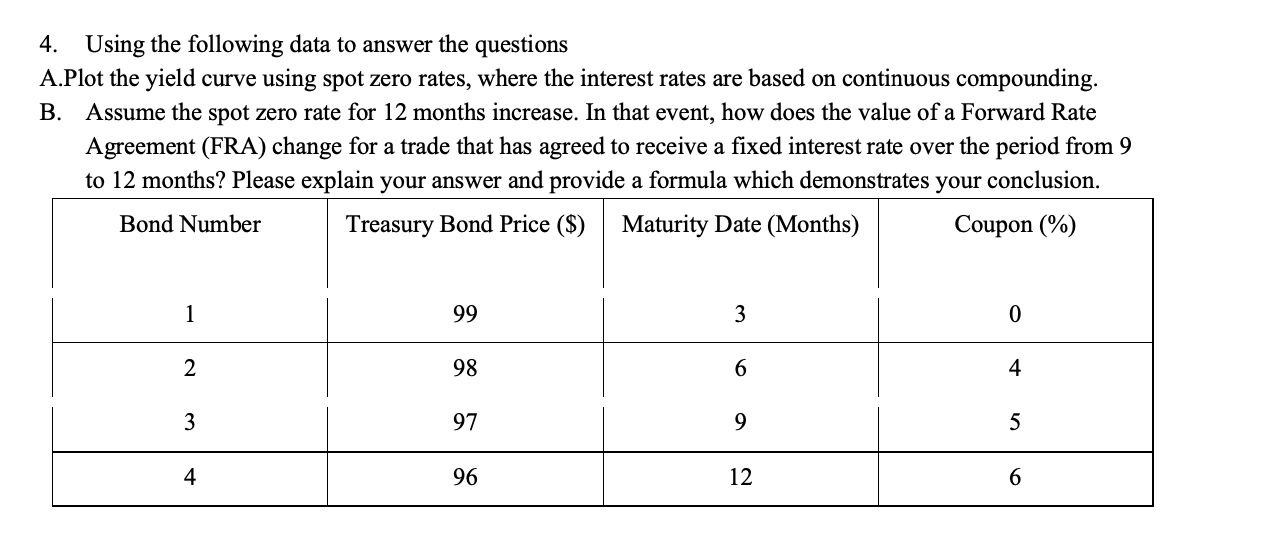

4. Using the following data to answer the questions A.Plot the yield curve using spot zero rates, where the interest rates are based on continuous compounding. B. Assume the spot zero rate for 12 months increase. In that event, how does the value of a Forward Rate Agreement (FRA) change for a trade that has agreed to receive a fixed interest rate over the period from 9 to 12 months? Please explain your answer and provide a formula which demonstrates your conclusion. Bond Number Treasury Bond Price ($) Maturity Date (Months) Coupon (%) 1 99 3 0 2 98 6 4 3 97 9 5 4 96 12 6

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock