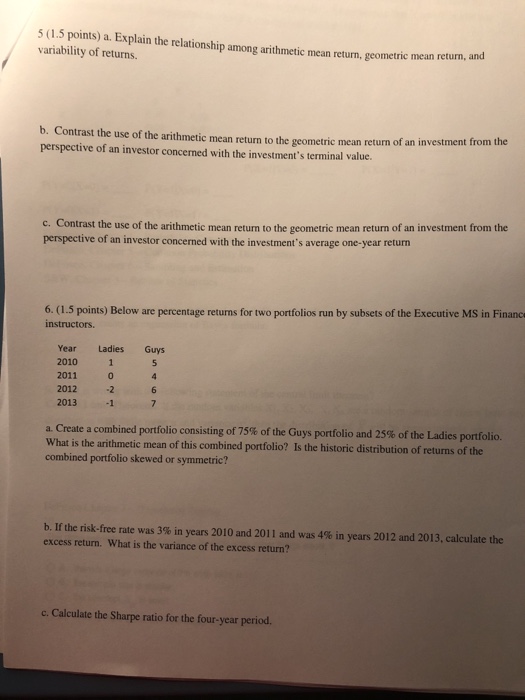

Question: 5 (1.5 points) a. Explain the relationship among arithmetic mean return, geometric variability of returns. metric mean return, and b. Contrast the use of the

5 (1.5 points) a. Explain the relationship among arithmetic mean return, geometric variability of returns. metric mean return, and b. Contrast the use of the arithmetic mean return to the geometric mean return of an investment f perspective of an investor concerned with the investment's terminal value. c. Contrast the use of the arithmetic mean return to the geometric mean return of an investment from the perspective of an investor concerned with the investment's average one-year return 6. (1.5 points) Below are percentage returns for two portfolios run by subsets of the Executive MS in Finance instructors Year Ladies Guys 2010 1 2011 0 2012 2 2013 1 a Create a combined portfolio consisting of 75% of the Guys portfolio and 25% of the Ladies portfolio. What is the arithmetic mean of this combined portfolio? Is the historic distribution of returns of the combined portfolio skewed or symmetric? b. If the risk-free rate was 3% in years 2010 and 2011 and was 4% in years 2012 and 2013, calculate the excess return. What is the variance of the excess return? c. Calculate the Sharpe ratio for the four-year period

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts