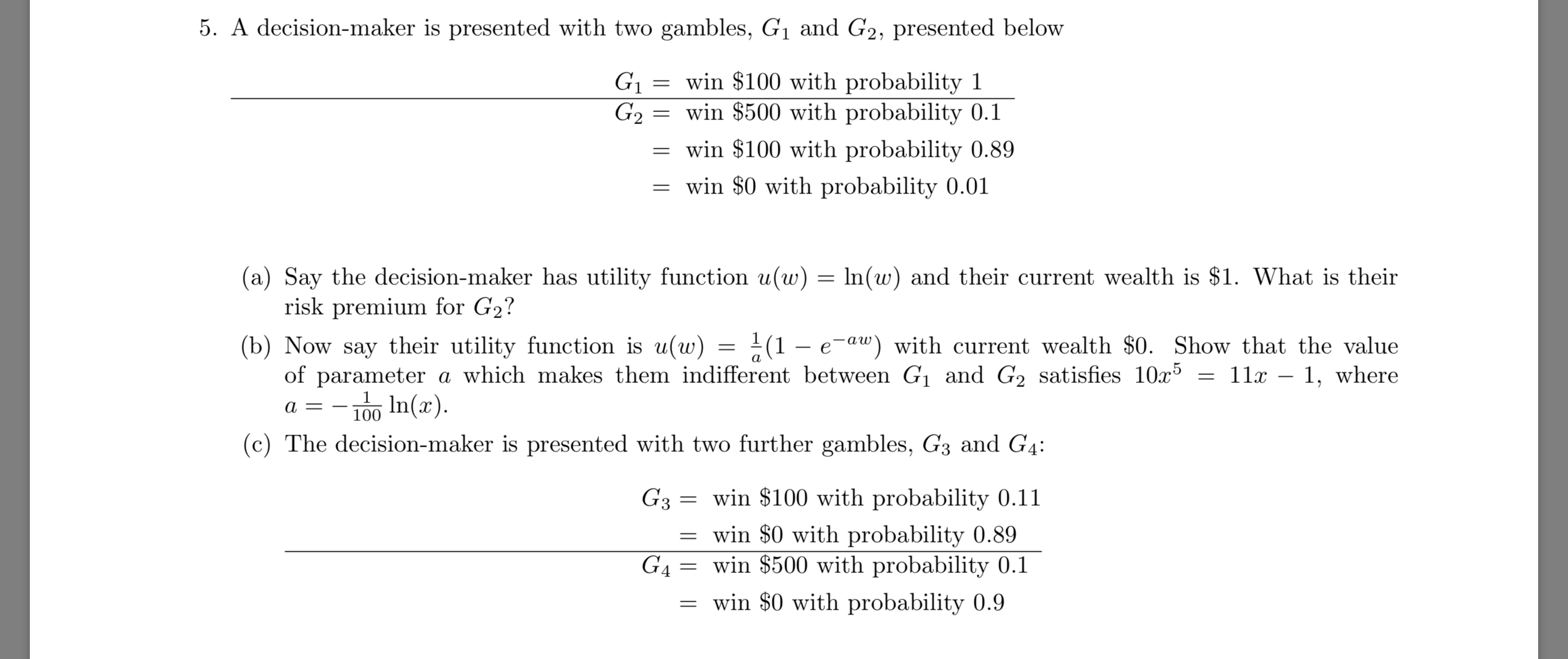

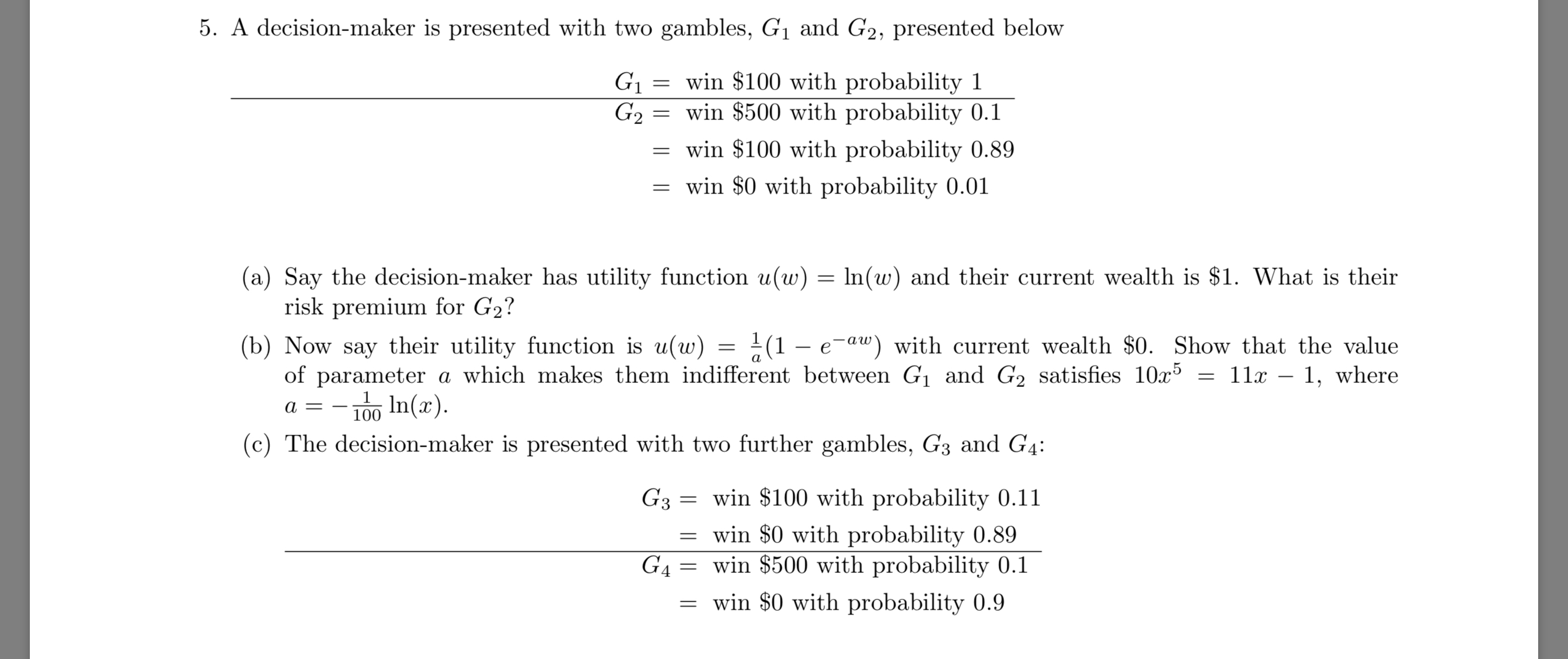

Question: 5. A decisionmaker is presented with two gambles, G1 and G2, presented below G1 02 ll ll win $100 with probability 1 win $500 with

5. A decisionmaker is presented with two gambles, G1 and G2, presented below G1 02 ll ll win $100 with probability 1 win $500 with probability 0.1 win $100 with probability 0.89 win $0 with probability 0.01 (a) Say the decision-maker has utility function u(w) = ln(w) and their current wealth is $1. What is their risk premium for G2? (b) Now say their utility function is u(w) = %(1 i e'm") with current wealth $0. Show that the value of parameter a which makes them indifferent between G1 and G2 satises 10905 = 11:20 i 1, where a = ln(x). (c) The decision-maker is presented with two further gambles, G3 and G4: G:3 win $100 with probability 0.11 win $0 with probability 0.89 win $500 with probability 0.1 G4 win $0 with probability 0.9 Show that a decision-maker who prefers G1 to G2 and G4 to 03 is not \"rational\" according to the Von NeumannMorgenstern axioms. Compare this result to your own, true preferences when comparing G1 to G2 and G3 to G4. Which axiom in particular is violated when the decisionmaker has this preference (i.e. preferring G1 to 02 and G4 to 6'3)? THE END

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts