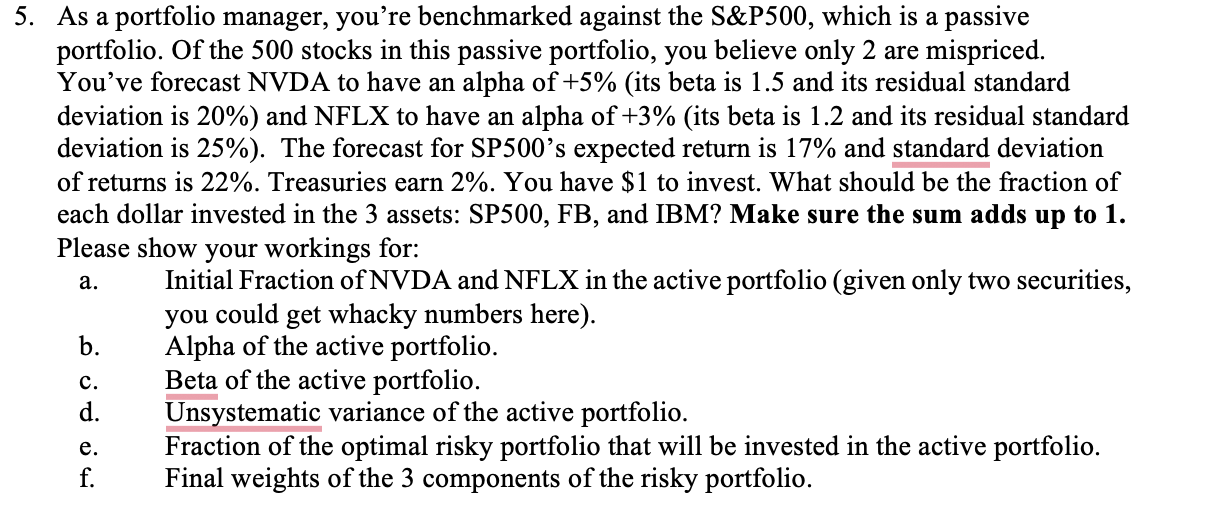

5. As a portfolio manager, you're benchmarked against the S&P500, which is a passive portfolio. Of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: