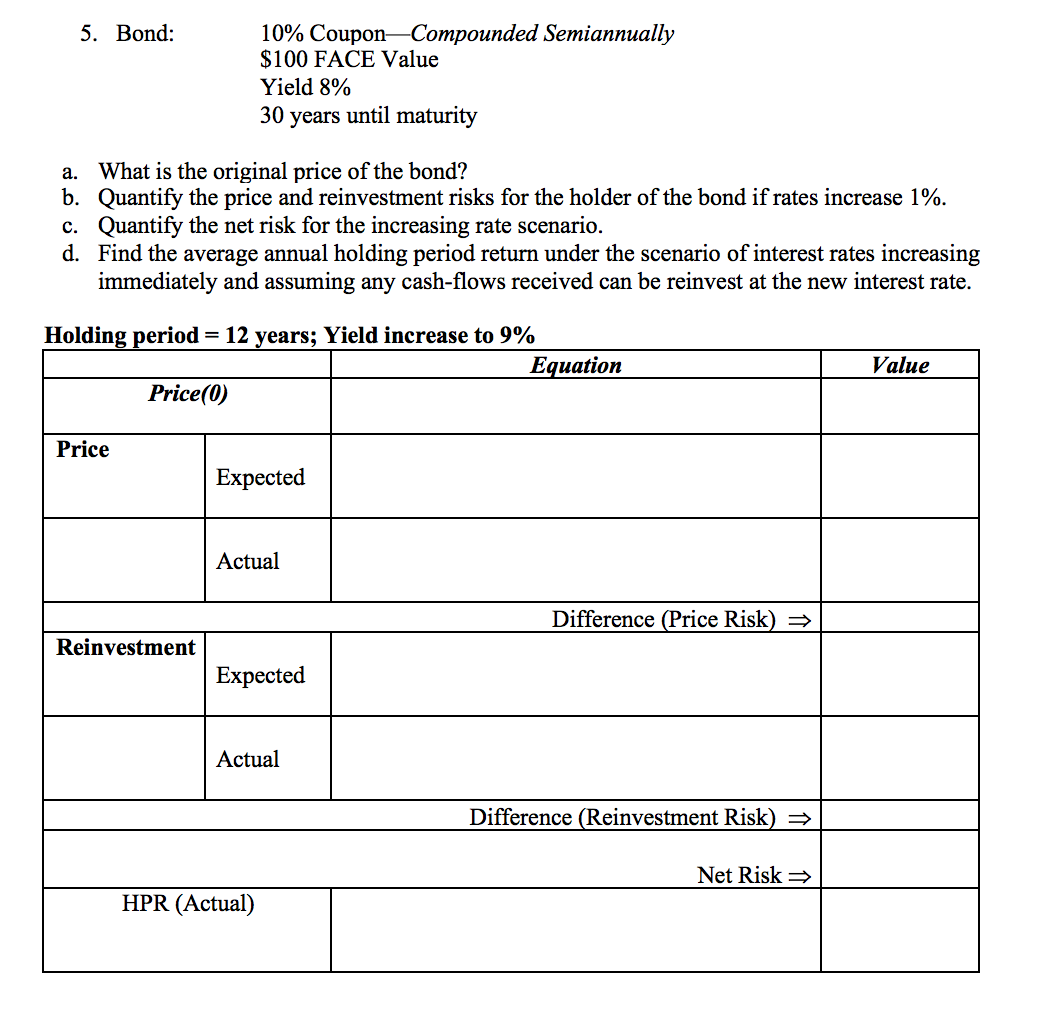

Question: 5. Bond: 10% Coupon -Compounded Semiannually $100 FACE Value Yield 8% 30 years until maturity a. What is the original price of the bond? b.

5. Bond: 10% Coupon -Compounded Semiannually $100 FACE Value Yield 8% 30 years until maturity a. What is the original price of the bond? b. Quantify the price and reinvestment risks for the holder of the bond if rates increase 1%. c. Quantify the net risk for the increasing rate scenario. d. Find the average annual holding period return under the scenario of interest rates increasing immediately and assuming any cash-flows received can be reinvest at the new interest rate. Holding period = 12 years; Yield increase to 9% Equation Price(0) Value Price Expected Actual Difference (Price Risk) = Reinvestment Expected Actual Difference (Reinvestment Risk) = Net sk HPR (Actual) 5. Bond: 10% Coupon -Compounded Semiannually $100 FACE Value Yield 8% 30 years until maturity a. What is the original price of the bond? b. Quantify the price and reinvestment risks for the holder of the bond if rates increase 1%. c. Quantify the net risk for the increasing rate scenario. d. Find the average annual holding period return under the scenario of interest rates increasing immediately and assuming any cash-flows received can be reinvest at the new interest rate. Holding period = 12 years; Yield increase to 9% Equation Price(0) Value Price Expected Actual Difference (Price Risk) = Reinvestment Expected Actual Difference (Reinvestment Risk) = Net sk HPR (Actual)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts