Question: 5. Computing your liability - An auto insurance example Although car insurance is legally required by all states, the coverage provided by different policies can

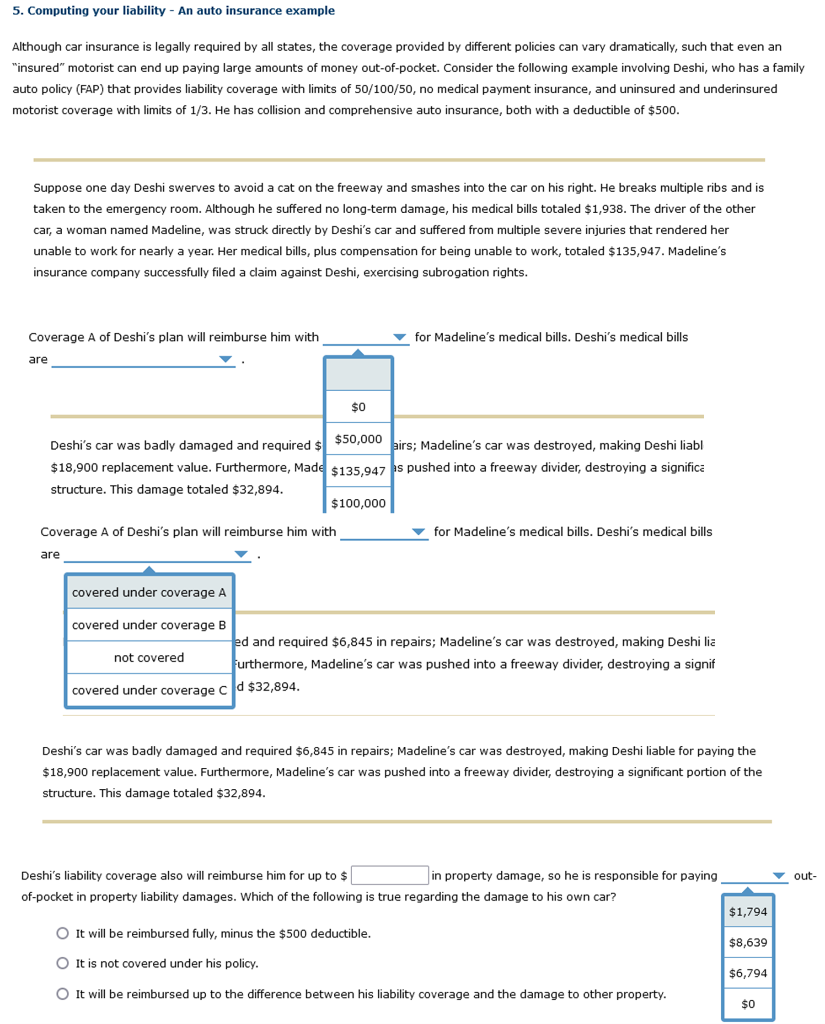

5. Computing your liability - An auto insurance example Although car insurance is legally required by all states, the coverage provided by different policies can vary dramatically, such that even an "insured" motorist can end up paying large amounts of money out-of-pocket. Consider the following example involving Deshi, who has a family auto policy (FAP) that provides liability coverage with limits of 50/100/50, no medical payment insurance, and uninsured and underinsured motorist coverage with limits of 1/3. He has collision and comprehensive auto insurance, both with a deductible of $500. Suppose one day Deshi swerves to avoid a cat on the freeway and smashes into the car on his right. He breaks multiple ribs and is taken to the emergency room. Although he suffered no long-term damage, his medical bills totaled $1,938. The driver of the other car, a woman named Madeline, was struck directly by Deshi's car and suffered from multiple severe injuries that rendered her unable to work for nearly a year. Her medical bills, plus compensation for being unable to work, totaled $135,947. Madeline's insurance company successfully filed a claim against Deshi, exercising subrogation rights. $18,900 replacement value. Furthermore, Madeline's car was pushed into a freeway divider, destroying a significant portion of the structure. This damage totaled $32,894. Deshi's liability coverage also will reimburse him for up to \$ in property damage, so he is responsible for paying of-pocket in property liability damages. Which of the following is true regarding the damage to his own car? It will be reimbursed fully, minus the $500 deductible. It is not covered under his policy. It will be reimbursed up to the difference between his liability coverage and the damage to other property. 5. Computing your liability - An auto insurance example Although car insurance is legally required by all states, the coverage provided by different policies can vary dramatically, such that even an "insured" motorist can end up paying large amounts of money out-of-pocket. Consider the following example involving Deshi, who has a family auto policy (FAP) that provides liability coverage with limits of 50/100/50, no medical payment insurance, and uninsured and underinsured motorist coverage with limits of 1/3. He has collision and comprehensive auto insurance, both with a deductible of $500. Suppose one day Deshi swerves to avoid a cat on the freeway and smashes into the car on his right. He breaks multiple ribs and is taken to the emergency room. Although he suffered no long-term damage, his medical bills totaled $1,938. The driver of the other car, a woman named Madeline, was struck directly by Deshi's car and suffered from multiple severe injuries that rendered her unable to work for nearly a year. Her medical bills, plus compensation for being unable to work, totaled $135,947. Madeline's insurance company successfully filed a claim against Deshi, exercising subrogation rights. $18,900 replacement value. Furthermore, Madeline's car was pushed into a freeway divider, destroying a significant portion of the structure. This damage totaled $32,894. Deshi's liability coverage also will reimburse him for up to \$ in property damage, so he is responsible for paying of-pocket in property liability damages. Which of the following is true regarding the damage to his own car? It will be reimbursed fully, minus the $500 deductible. It is not covered under his policy. It will be reimbursed up to the difference between his liability coverage and the damage to other property

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts