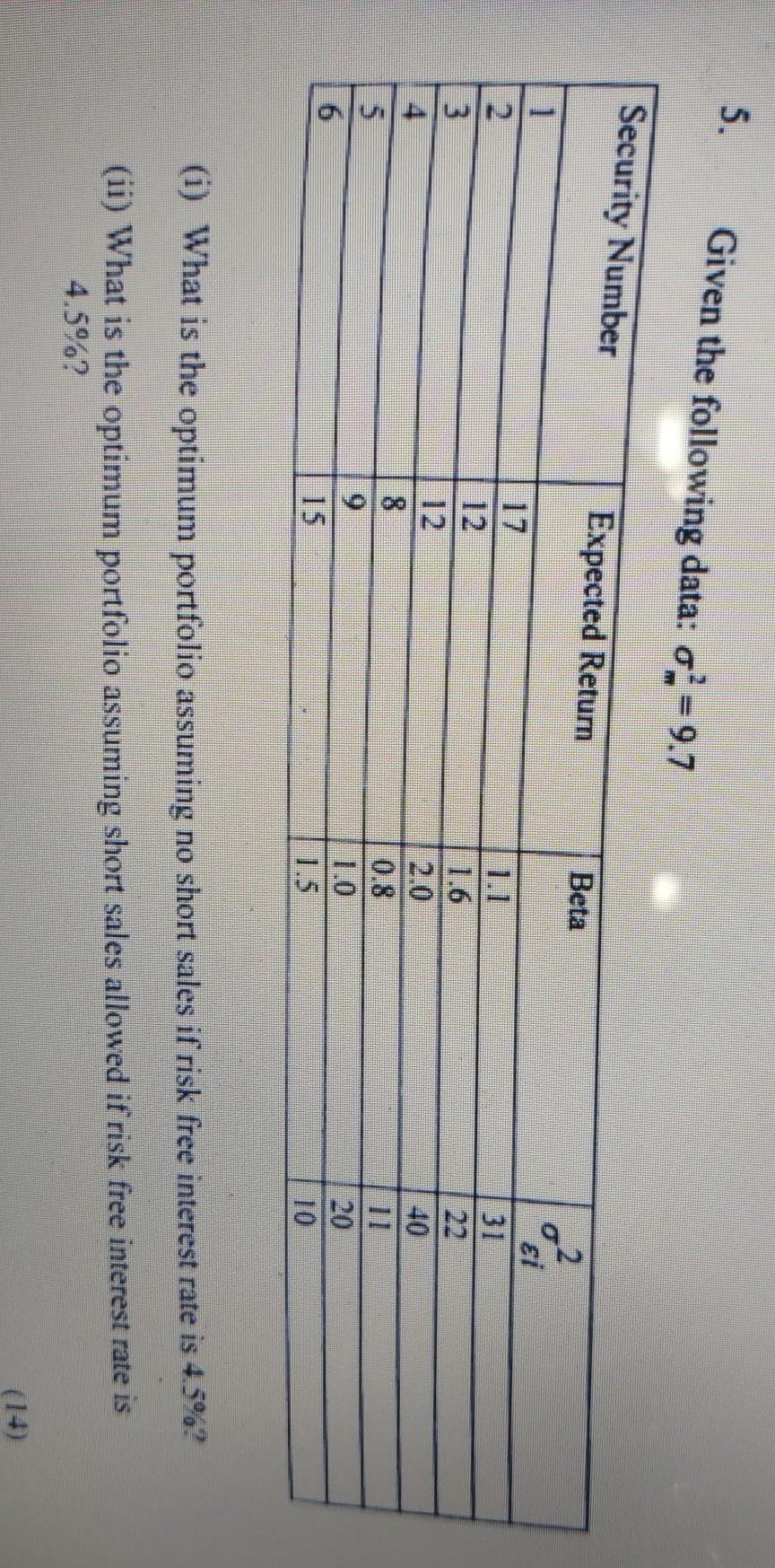

Question: 5. Given the following data. o? = 9.7 Security Number Expected Retum Beta 1 2 3 2 ei 31 1.1 1.6 40 5 6 8

5. Given the following data. o? = 9.7 Security Number Expected Retum Beta 1 2 3 2 ei 31 1.1 1.6 40 5 6 8 9 (i) What is the optimum portfolio assuming no short sales if risk free interest rate is 4.5%? (ii) What is the optimum portfolio assuming short sales allowed if risk free interest rate is 4.5%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock