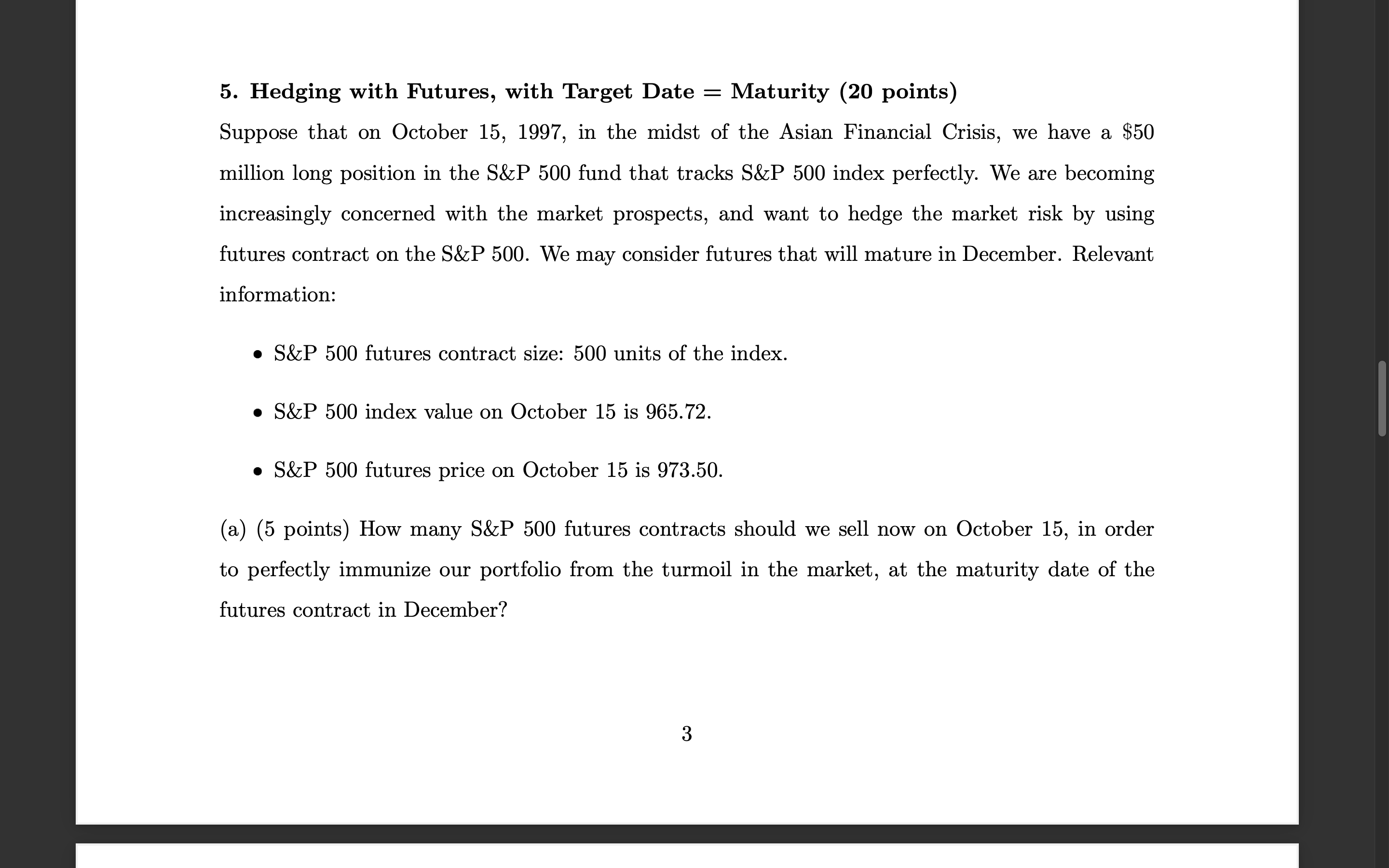

Question: 5. Hedging with Futures, with Target Date = Maturity (20 points) Suppose that on October 15, 1997, in the midst of the Asian Financial Crisis,

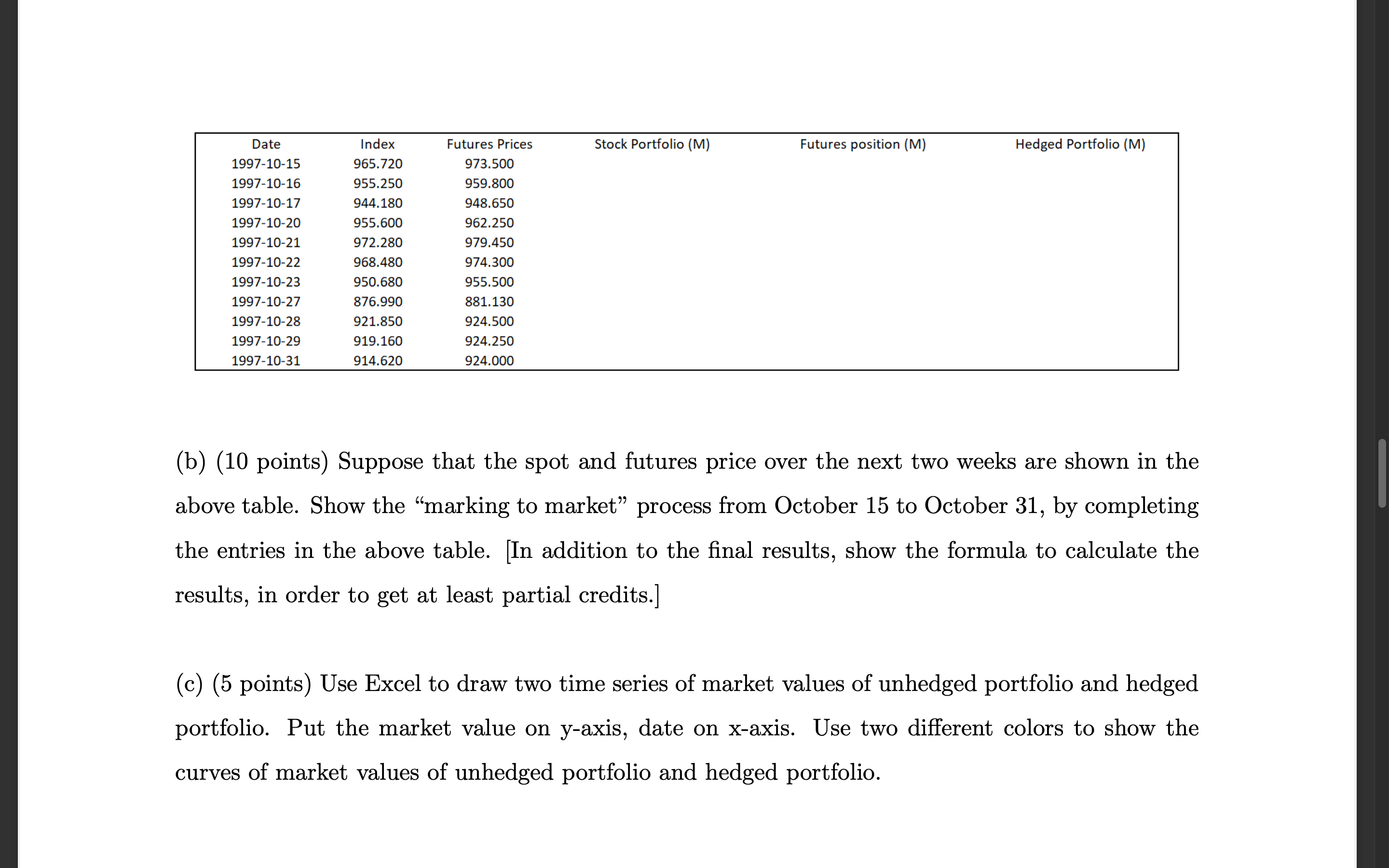

5. Hedging with Futures, with Target Date = Maturity (20 points) Suppose that on October 15, 1997, in the midst of the Asian Financial Crisis, we have a $50 million long position in the S\&P 500 fund that tracks S\&P 500 index perfectly. We are becoming increasingly concerned with the market prospects, and want to hedge the market risk by using futures contract on the S\&P 500. We may consider futures that will mature in December. Relevant information: - S&P500 futures contract size: 500 units of the index. - S&P500 index value on October 15 is 965.72 . - S&P500 futures price on October 15 is 973.50 . (a) (5 points) How many S\&P 500 futures contracts should we sell now on October 15, in order to perfectly immunize our portfolio from the turmoil in the market, at the maturity date of the futures contract in December? (b) (10 points) Suppose that the spot and futures price over the next two weeks are shown in the above table. Show the "marking to market" process from October 15 to October 31, by completing the entries in the above table. [In addition to the final results, show the formula to calculate the results, in order to get at least partial credits.] (c) (5 points) Use Excel to draw two time series of market values of unhedged portfolio and hedged portfolio. Put the market value on y-axis, date on x-axis. Use two different colors to show the curves of market values of unhedged portfolio and hedged portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts