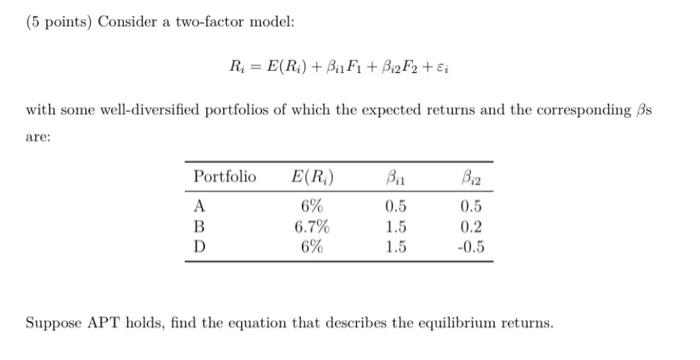

Question: (5 points) Consider a two-factor model: R = E(R) + BF1 + B2F2 + Ei with some well-diversified portfolios of which the expected returns and

(5 points) Consider a two-factor model: R = E(R) + BF1 + B2F2 + Ei with some well-diversified portfolios of which the expected returns and the corresponding 3s are: Portfolio E(R) Bil B12 A 6% 0.5 0.5 B 6.7% 1.5 0.2 D 6% 1.5 -0.5 Suppose APT holds, find the equation that describes the equilibrium returns

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock